The SSAS 50% LTV Cap Explained

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

What Is the SSAS 50% LTV Cap?

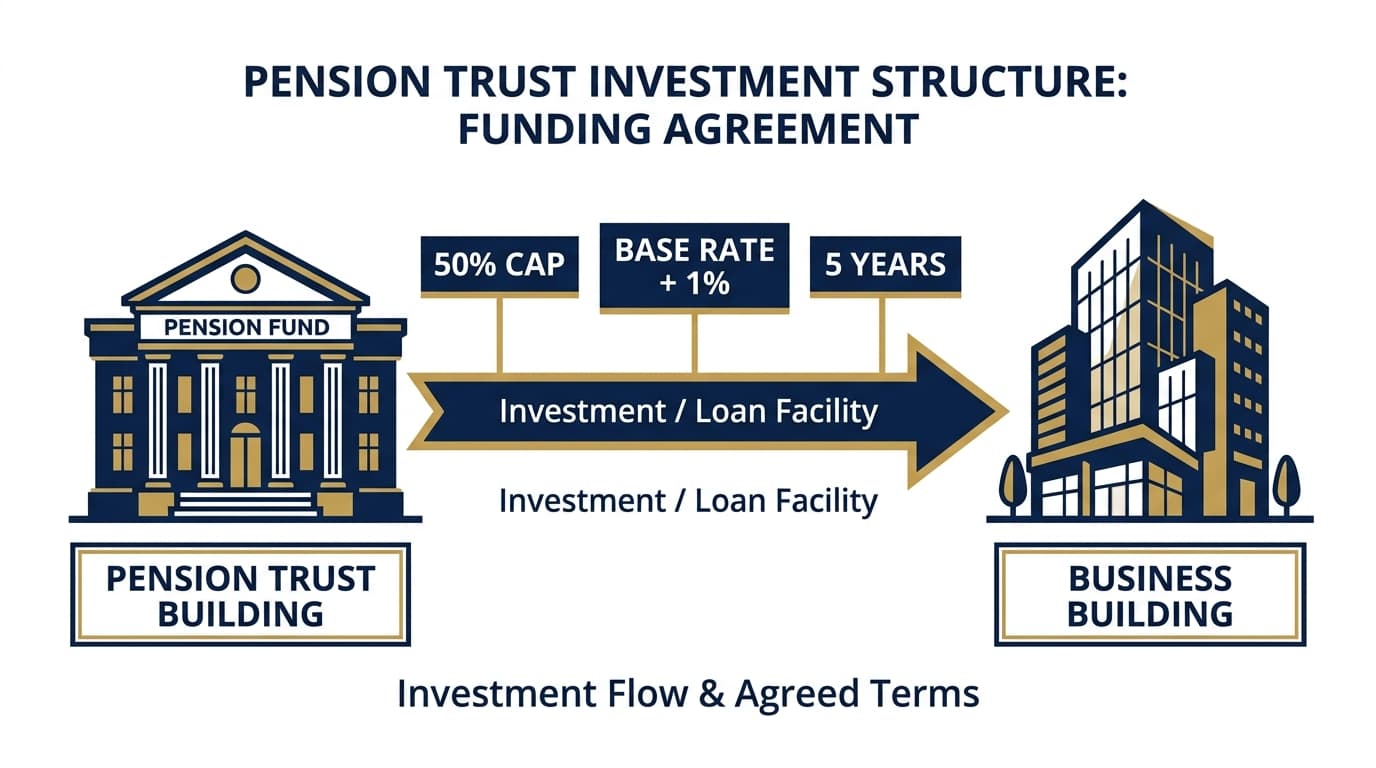

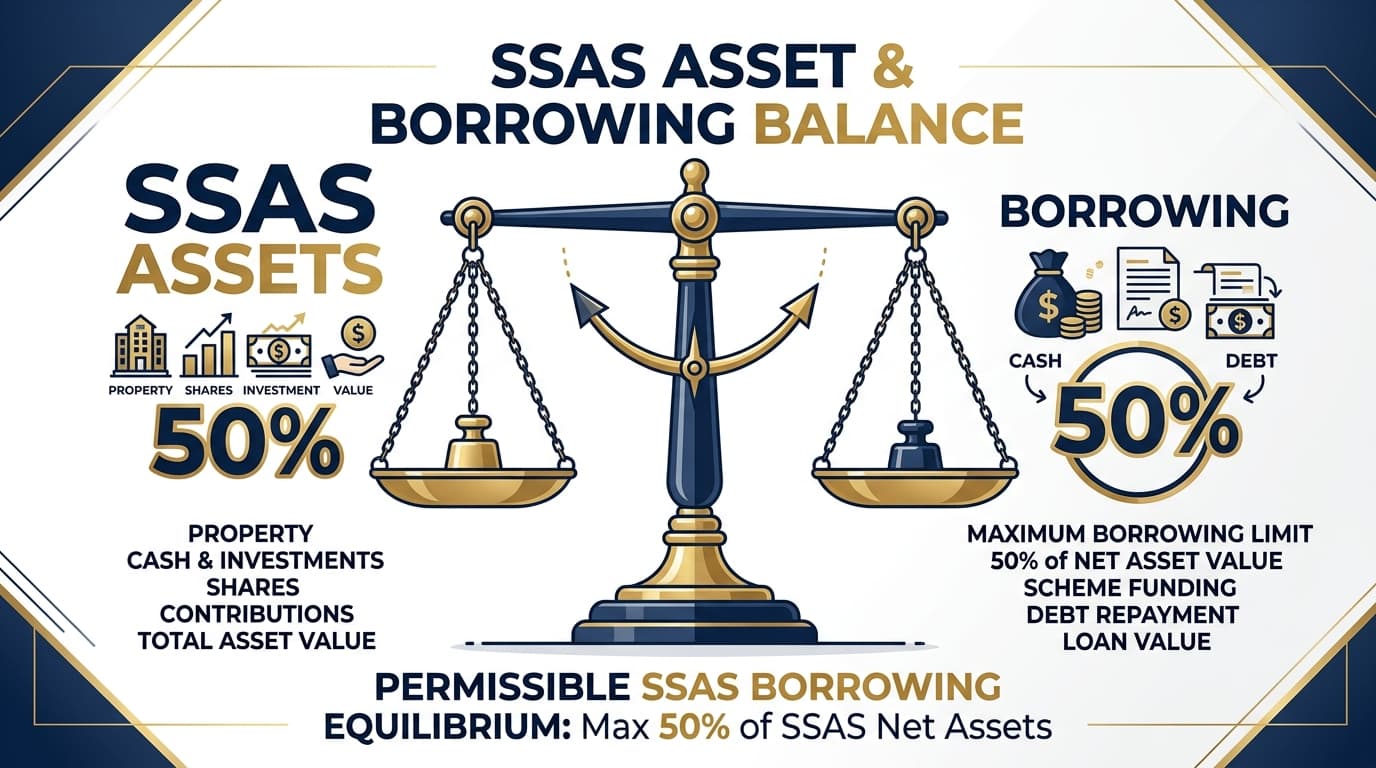

Every Small Self-Administered Scheme (SSAS) pension is permitted to borrow money to invest — but that borrowing is tightly controlled by HMRC rules. The most fundamental constraint is the 50% loan-to-value (LTV) cap, which limits how much your scheme can borrow relative to the net value of its assets.

In plain terms: your SSAS cannot have outstanding borrowing that exceeds 50% of the scheme's total net asset value. Get this wrong, and your scheme risks being deemed non-compliant, which can trigger serious tax consequences for all members.

In our experience working with SSAS trustees across the UK, this single rule causes more confusion than any other. Trustees often misunderstand what "net asset value" means, what counts as borrowing, and how the calculation changes when property values move.

How the 50% LTV Calculation Actually Works

The calculation sounds simple but has important nuances. HMRC defines the limit as follows:

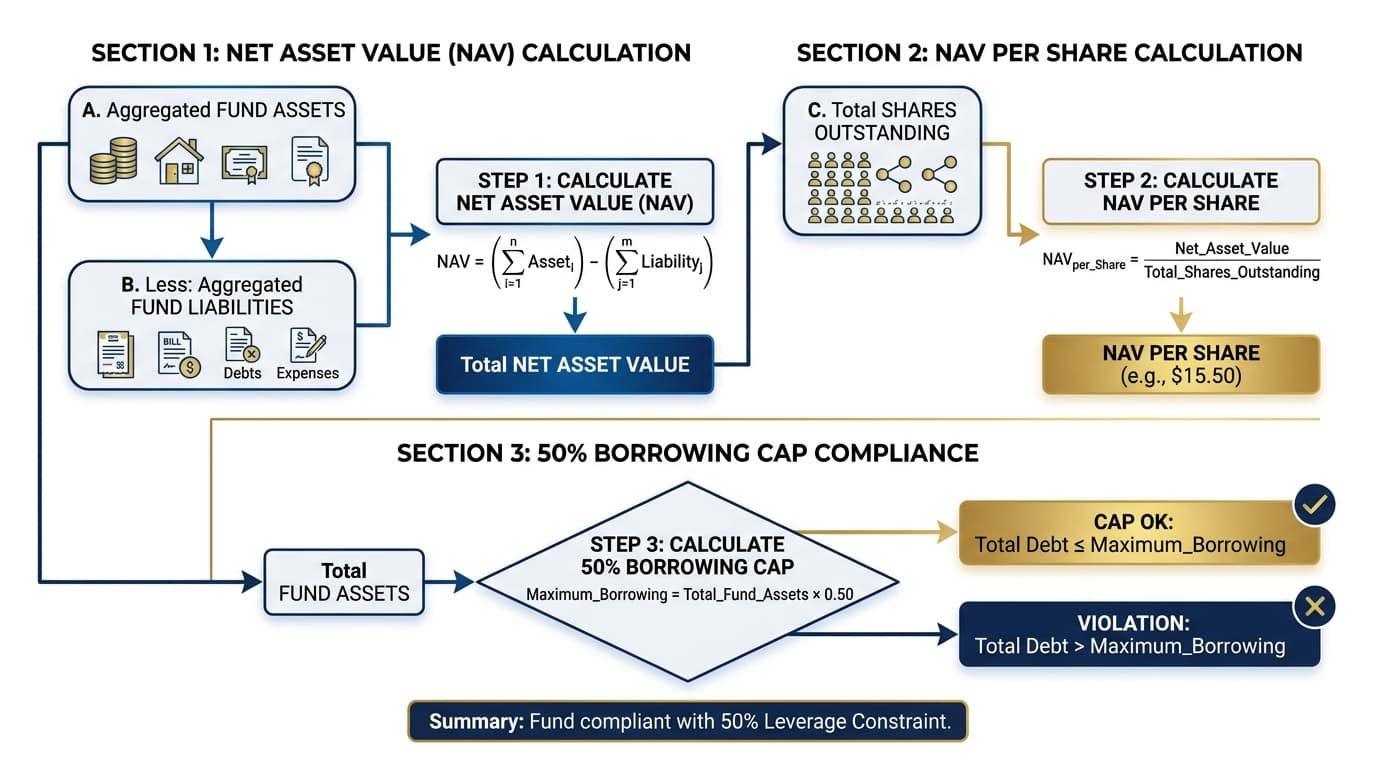

Total borrowing outstanding must not exceed 50% of the net market value of all scheme assets at the time of the borrowing.

Let's break that down:

- Total borrowing: This includes all outstanding loans taken by the SSAS — not just property mortgages. Any loanback to the sponsoring employer, bridging loans, or other finance facilities all count.

- Net market value: The current market value of all assets, minus any existing liabilities. This includes the property itself (at market value, not purchase price), cash holdings, and any other investments held by the scheme.

- At the time of borrowing: The test is applied when the new borrowing is taken, not on an ongoing basis. However, if your scheme value subsequently falls, your scheme could be technically in breach — which is why lenders typically apply more conservative LTV ratios.

A Worked Example

Suppose your SSAS has the following assets:

- Commercial property (market value): £600,000

- Cash in the scheme bank account: £150,000

- Existing mortgage on the property: £200,000

Total asset value = £750,000. Existing liabilities = £200,000. Net asset value = £550,000.

Maximum permissible borrowing = 50% × £550,000 = £275,000.

Since £200,000 is already drawn, the SSAS can borrow an additional £75,000 before hitting the cap.

For a deeper look at how borrowing capacity is calculated, see our guide on SSAS borrowing power calculation.

What Counts as Borrowing?

This is where many SSAS trustees make costly mistakes. The following all count towards your borrowing limit:

- Commercial mortgages secured against property held by the SSAS

- Bridging loans used to acquire property prior to term finance

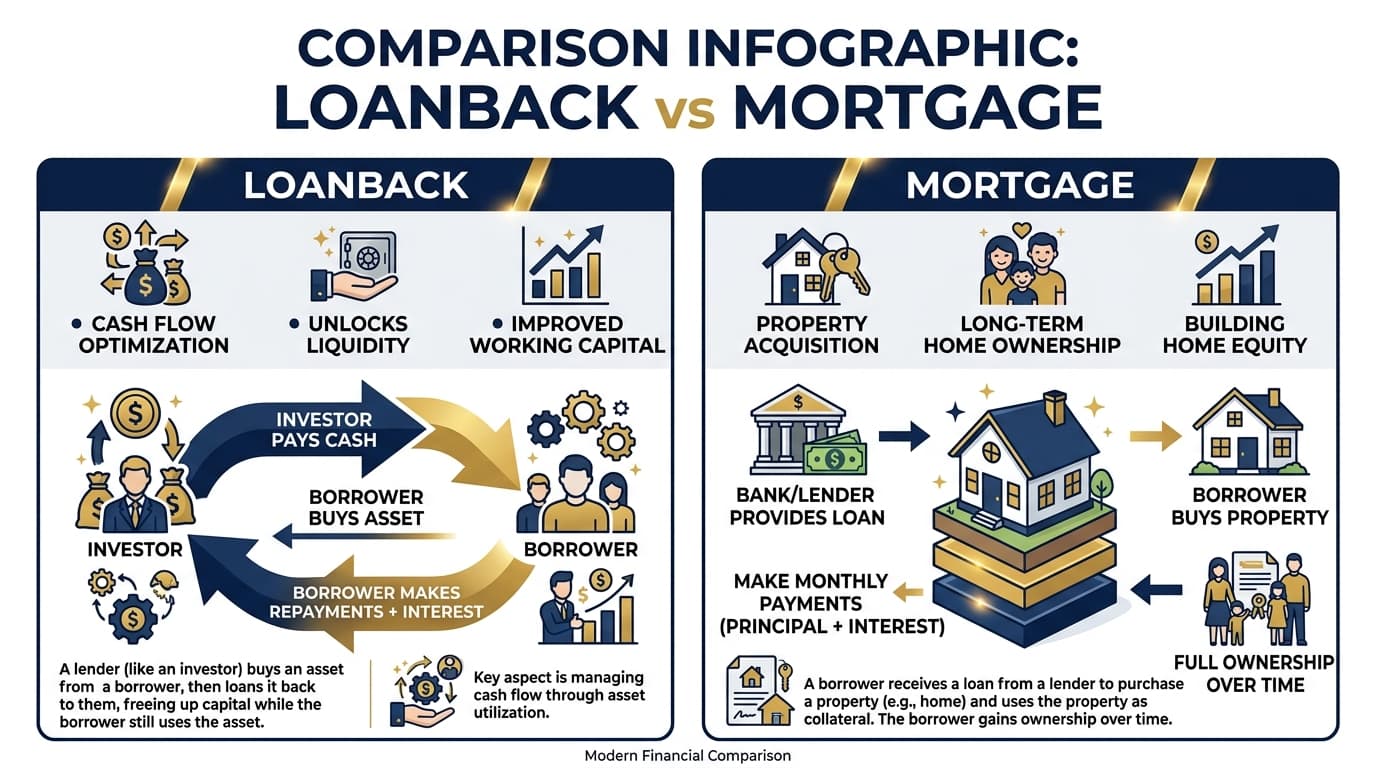

- Loanbacks to the sponsoring employer (subject to separate HMRC rules — see our loanback guide)

- Any other secured or unsecured borrowing by the scheme

What does NOT count:

- Deferred payment arrangements that are genuinely commercial

- Normal trade payables (e.g., professional fees outstanding)

Matt Lenzie notes: "We regularly see SSAS trustees who've arranged both a property mortgage and a loanback without checking whether the combined borrowing still sits within the 50% cap. Both transactions may individually appear fine, but together they breach the limit."

Why Lenders Apply More Conservative LTVs

While HMRC permits borrowing up to 50% of net asset value, most specialist SSAS lenders won't lend at 50% LTV against the property itself. The distinction matters:

- The HMRC cap is 50% of total net scheme assets

- Individual lender LTV ratios typically range from 65-75% against the property being purchased, but the total scheme borrowing must still stay within the HMRC 50% cap

In practice, lenders will run their own checks to ensure the HMRC limit isn't breached before agreeing to lend. They may require a statement of scheme assets from your pension administrator to verify this.

To understand what lenders look for, visit our lender panel or explore SSAS property finance options.

What Happens If the Cap Is Breached?

If your SSAS borrows beyond the 50% cap, HMRC treats the excess borrowing as an "unauthorised payment" from the scheme. The consequences are severe:

- The amount of the unauthorised payment is subject to a tax charge of up to 40% (the "unauthorised payments charge")

- A further "surcharge" of 15% applies if the unauthorised payments exceed 25% of the fund value

- The scheme may face de-registration in extreme cases

- All members and the sponsoring employer may be jointly and severally liable

These penalties make it absolutely critical to calculate your headroom carefully before proceeding with any borrowing.

Managing the Cap as Your Scheme Grows

The good news is that as your scheme's assets grow — through contributions, investment returns, and property appreciation — your borrowing headroom expands. Many SSAS trustees find that their initial borrowing capacity grows significantly over time, allowing them to acquire additional properties or refinance at better rates.

Key tactics for managing the cap effectively:

- Instruct regular professional valuations of all property held by the scheme — updated values increase your headroom

- Monitor the outstanding balance on any loanbacks, as these reduce your capacity for property finance

- Keep your pension administrator informed of all planned transactions so they can model the cap calculation before you commit

- Consider the timing of member contributions, which increase scheme assets and therefore headroom

The 50% Cap and Loanbacks

One area that catches trustees off guard is the interaction between the HMRC borrowing cap and the loanback rules. Loanbacks — where the SSAS lends money to the sponsoring employer — are also capped at 50% of scheme assets, but this is a separate calculation from the borrowing cap.

However, since loanbacks are a form of scheme asset (a receivable), they affect the net asset value calculation used in the borrowing cap. In our experience, trustees with both property mortgages and loanbacks in place often have less capacity for additional borrowing than they expect.

Read more in our detailed guide to SSAS loanback vs mortgage options.

Key Takeaways

- The 50% cap applies to total outstanding borrowing as a percentage of net scheme assets — not just property mortgage LTV

- All forms of scheme borrowing count towards the cap, including loanbacks

- Breaching the cap triggers unauthorised payments tax charges that can be devastating for members

- Lenders will independently verify compliance with the cap before approving finance

- Regular professional valuations and close liaison with your SSAS administrator are essential

Ready to Explore SSAS Property Finance?

Understanding the 50% LTV cap is the foundation of structuring successful SSAS property transactions. If you'd like to discuss how much your scheme can borrow, or model a specific acquisition, our team can help.

Contact us today for a no-obligation conversation, or use our SSAS mortgage calculator to get an initial estimate of your borrowing capacity.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.