SSAS Property Finance Guides

Expert guides covering SSAS pensions, commercial property investment, HMRC compliance, and financing strategies. Written by Matt Lenzie, former banker and corporate finance partner.

100 guides

SSAS Long-Term Wealth Strategy: A 20-Year Framework

The full power of an SSAS commercial property strategy only becomes visible over a 15-20 year investment horizon. This guide sets out a comprehensive framework for each phase of that journey.

SSAS Property Investment for New Directors: Where to Begin

If you are a director who has just heard about SSAS pension property investment for the first time, this guide explains everything you need to know to understand whether it is right for you.

Combining Your SSAS with Other Investments: A Strategic Guide

An SSAS is a powerful wealth-building tool, but it works best as part of a broader investment strategy. This guide explores how to integrate your SSAS with ISAs, buy-to-let, business assets, and more.

SSAS Succession Planning: Protecting Wealth Across Generations

An SSAS is one of the most IHT-efficient wealth vehicles available to business owners. Succession planning ensures the value you have built passes to your chosen beneficiaries in the most tax-efficient way.

When to Sell Your SSAS Property: Timing the Exit

Deciding when to sell a commercial property held inside an SSAS requires balancing market conditions, lease events, retirement timelines, and portfolio strategy. This guide explains the key decision factors.

SSAS Property vs Equities: Which Delivers Better Pension Returns?

Property and equities are the two dominant SSAS investment strategies. This guide compares historical returns, risk profiles, tax treatment, and practical considerations for pension scheme trustees.

SSAS Property Exit Strategies: Planning Your Route to Liquidity

Every SSAS property investment has an eventual exit. Planning that exit well in advance of when you need it is the key to maximising returns and avoiding forced sales at the wrong time.

Generating Retirement Income from SSAS Property

As SSAS members approach retirement, the focus shifts from building the property portfolio to drawing income from it. This guide explains the options and the planning required.

SSAS Investment Diversification: Beyond Property

Commercial property is a powerful SSAS investment, but over-concentration in a single asset class carries real risks. This guide explains how to diversify intelligently within an SSAS structure.

Building a Commercial Property Portfolio Inside Your SSAS

Building a multi-property portfolio inside an SSAS requires more than just identifying good properties — it requires a coherent long-term strategy. This guide covers the principles and practicalities.

SSAS Mixed-Use Deal: A Worked Example

Mixed-use properties can offer attractive yields, but SSAS schemes cannot hold residential elements directly. This worked example shows how trustees structured a mixed-use acquisition to maximise returns while staying HMRC-compliant.

SSAS Warehouse Acquisition: A Complete Case Study

An SSAS trustee group acquired a £620,000 warehouse unit for occupation by their logistics business. This case study covers the full journey from market analysis to completion.

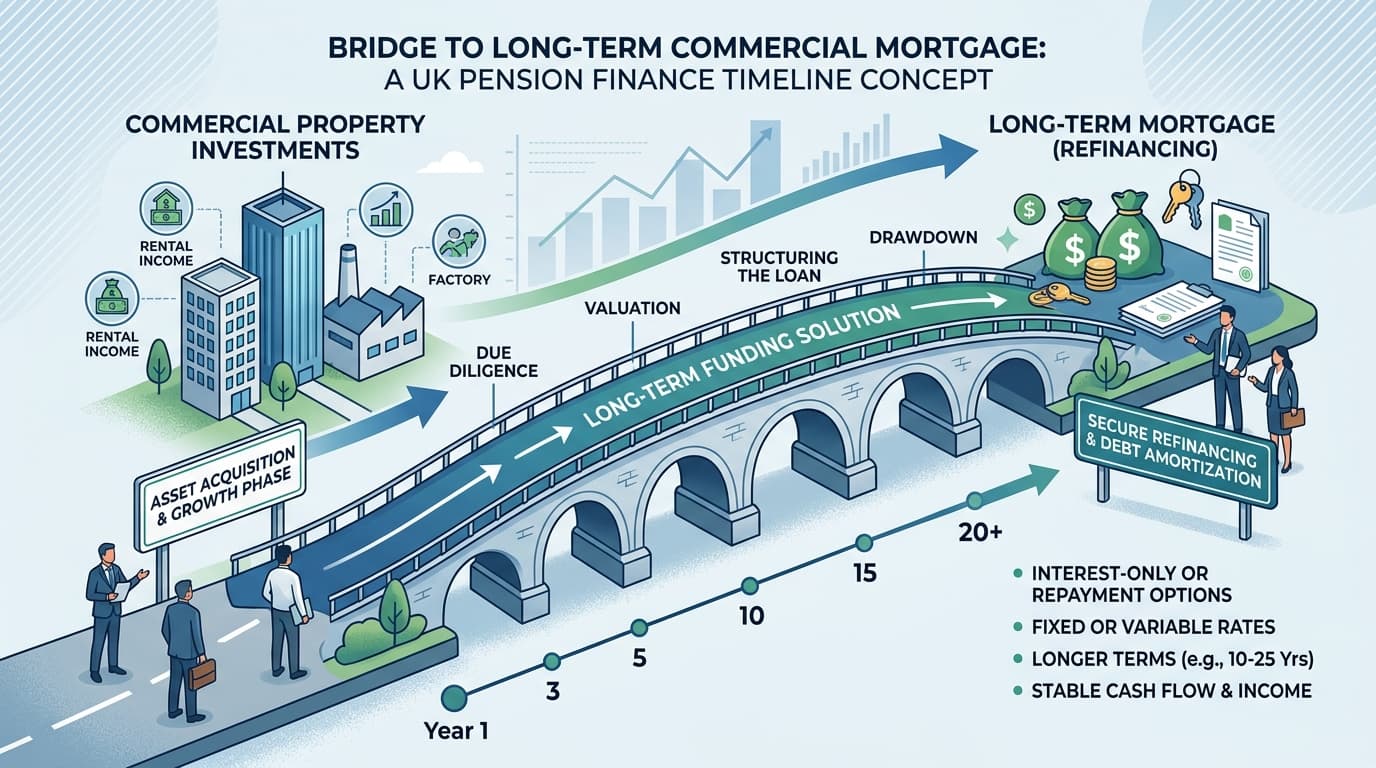

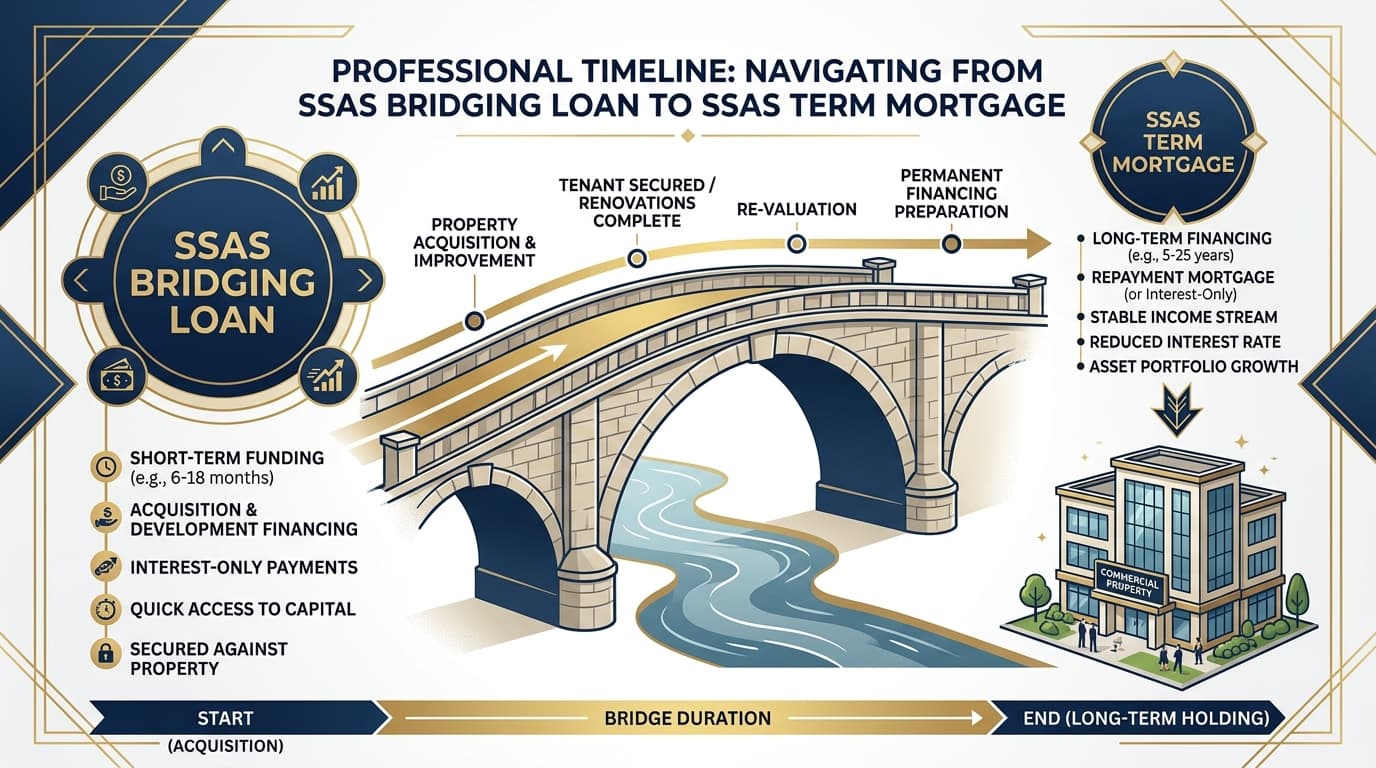

SSAS Bridging to Term: A Case Study

When a commercial property came to market at below market value but needed to complete in six weeks, this SSAS used bridging finance to secure the deal — then refinanced onto a term mortgage. Here is how it worked.

First-Time SSAS Property Purchase: A Complete Walkthrough

Making your first SSAS property purchase can feel daunting. This complete walkthrough explains every step — from setting up the scheme correctly through to completion and lease management.

SSAS Portfolio Building: A Long-Term Case Study

Over eight years, one SSAS grew from a single industrial unit to a three-property commercial portfolio worth £1.4 million. This case study traces each step of that journey.

Connected Party Lease Setup: A Step-by-Step Example

When an SSAS buys a property and leases it back to the sponsoring employer, a connected party lease must be set up correctly. This guide walks through every step of the process.

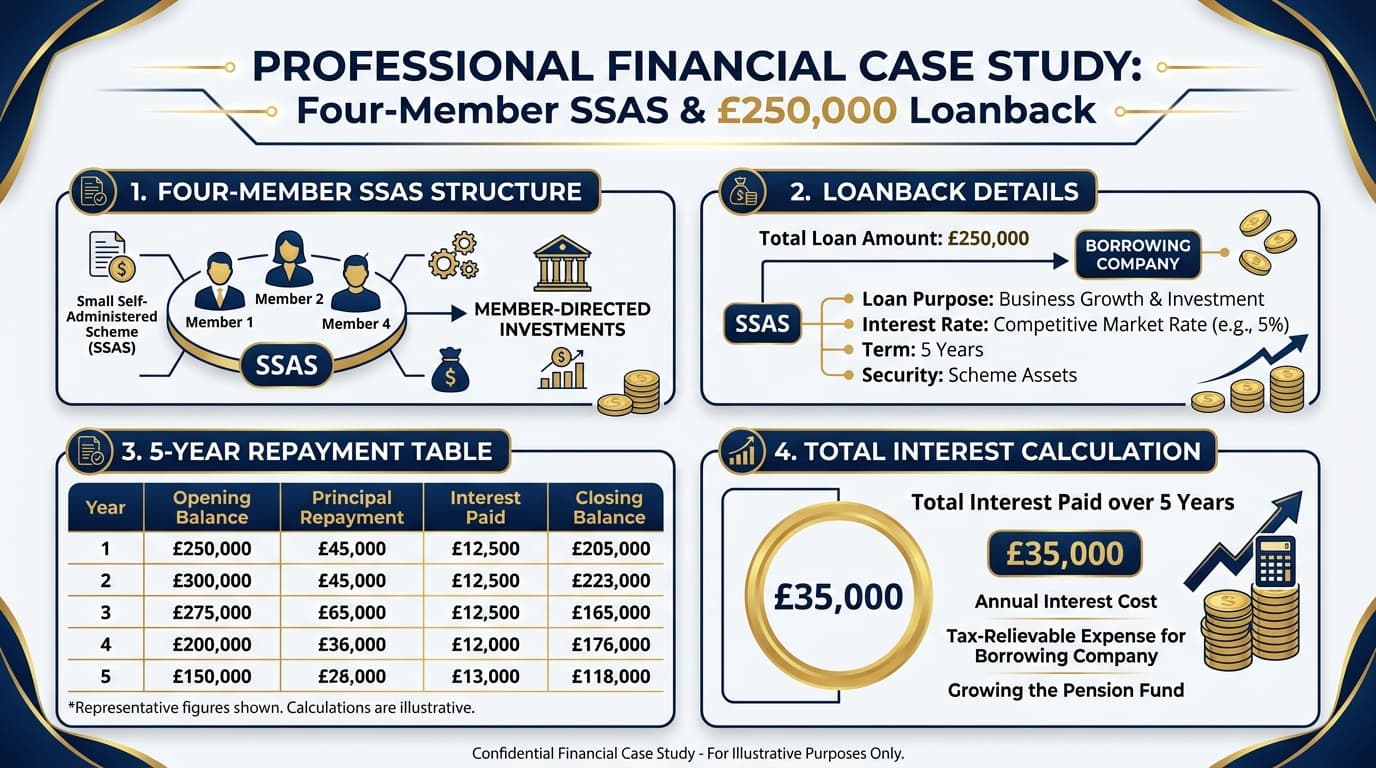

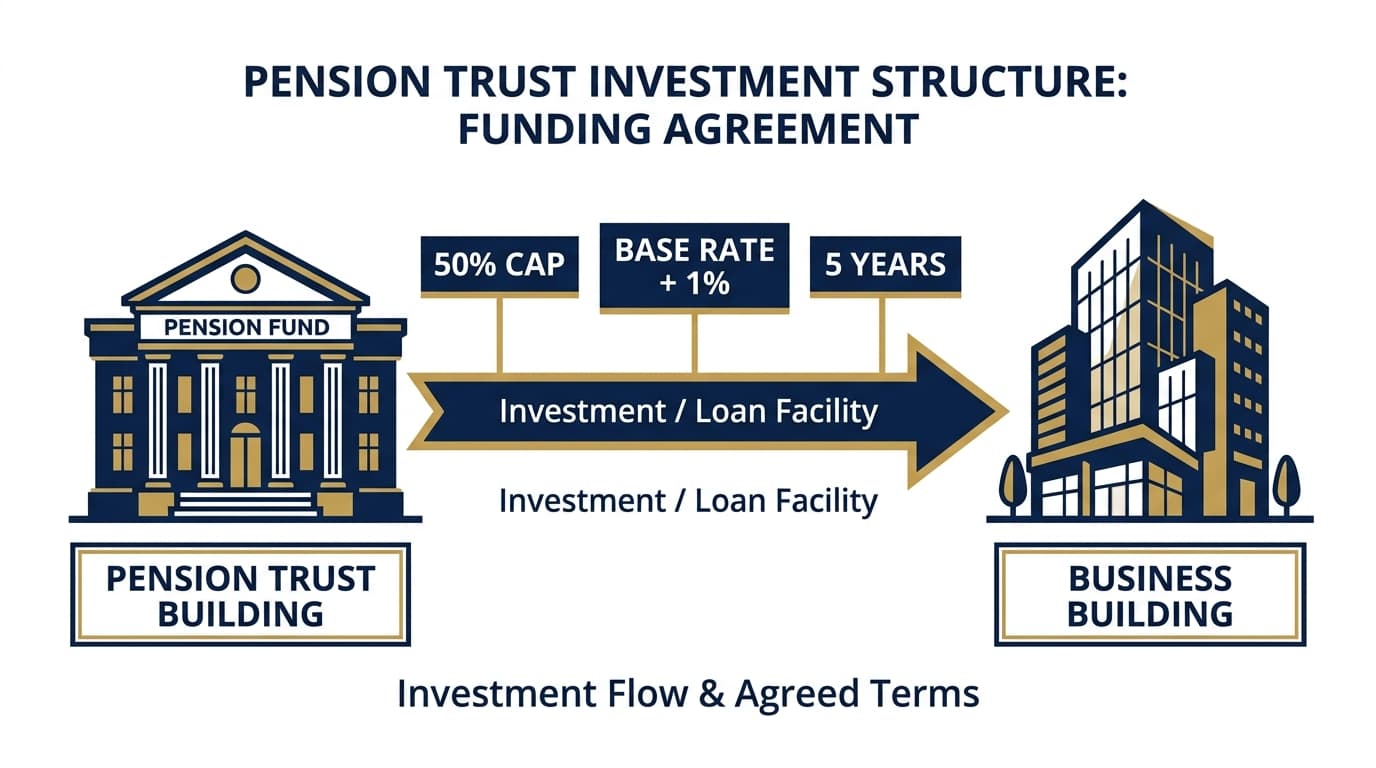

SSAS Loanback: A Detailed Worked Example

An SSAS can lend up to 50% of its net assets back to the sponsoring employer. This worked example shows how a £150,000 loanback was structured, what the rules require, and how the repayments work.

Multi-Member SSAS Fund Pooling: A Worked Example

When individual SSAS sub-funds are too small to act alone, members can pool their resources for a joint property purchase. This case study shows exactly how that works in practice.

SSAS Industrial Unit Refinance: A Step-by-Step Example

An SSAS already owned an industrial unit outright. By refinancing it, the trustees released £180,000 to fund additional member contributions and diversify investments. Here is how it worked.

SSAS Office Purchase: A £500k Worked Example

Walk through a real-world scenario where an SSAS trustee group purchases a £500,000 commercial office unit — from initial fund pooling through to completion and leaseback.

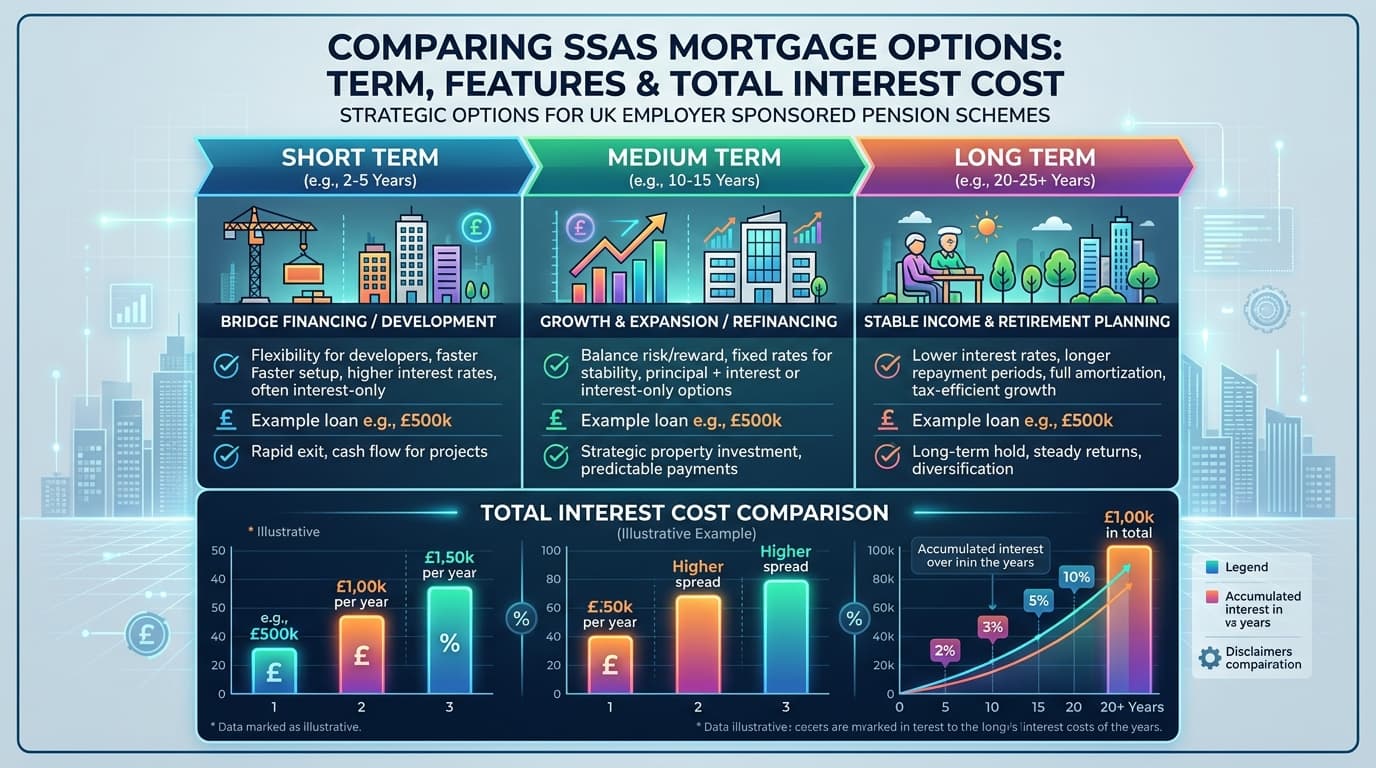

SSAS Mortgage Term Options: Choosing the Right Length

SSAS mortgage terms typically run from five to twenty-five years. Choosing the right term involves balancing monthly cost, total interest, flexibility, and your scheme's retirement horizon.

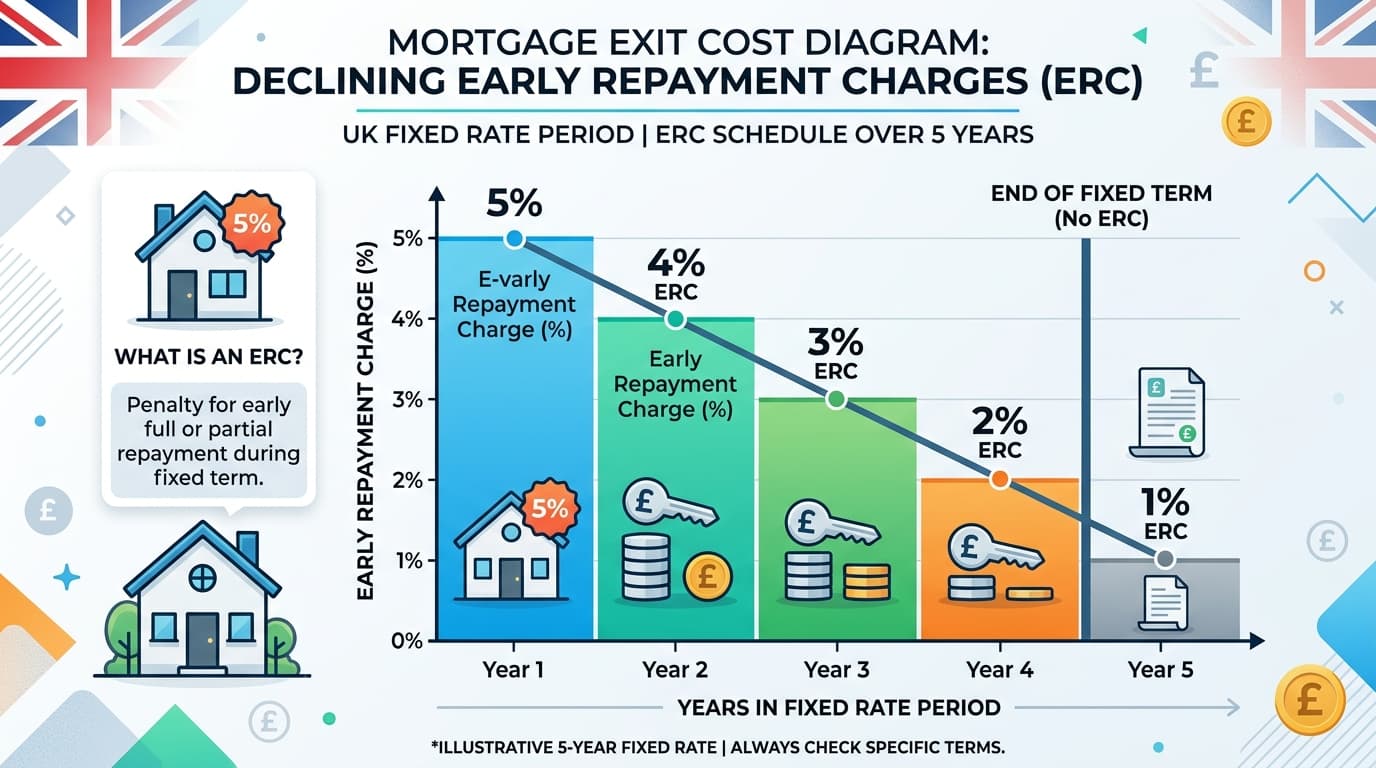

SSAS Exit Fees Explained: What You Pay When Leaving a Mortgage

Exit fees and early repayment charges can significantly affect the true cost of your SSAS mortgage. Here is what to look for and how to plan around them.

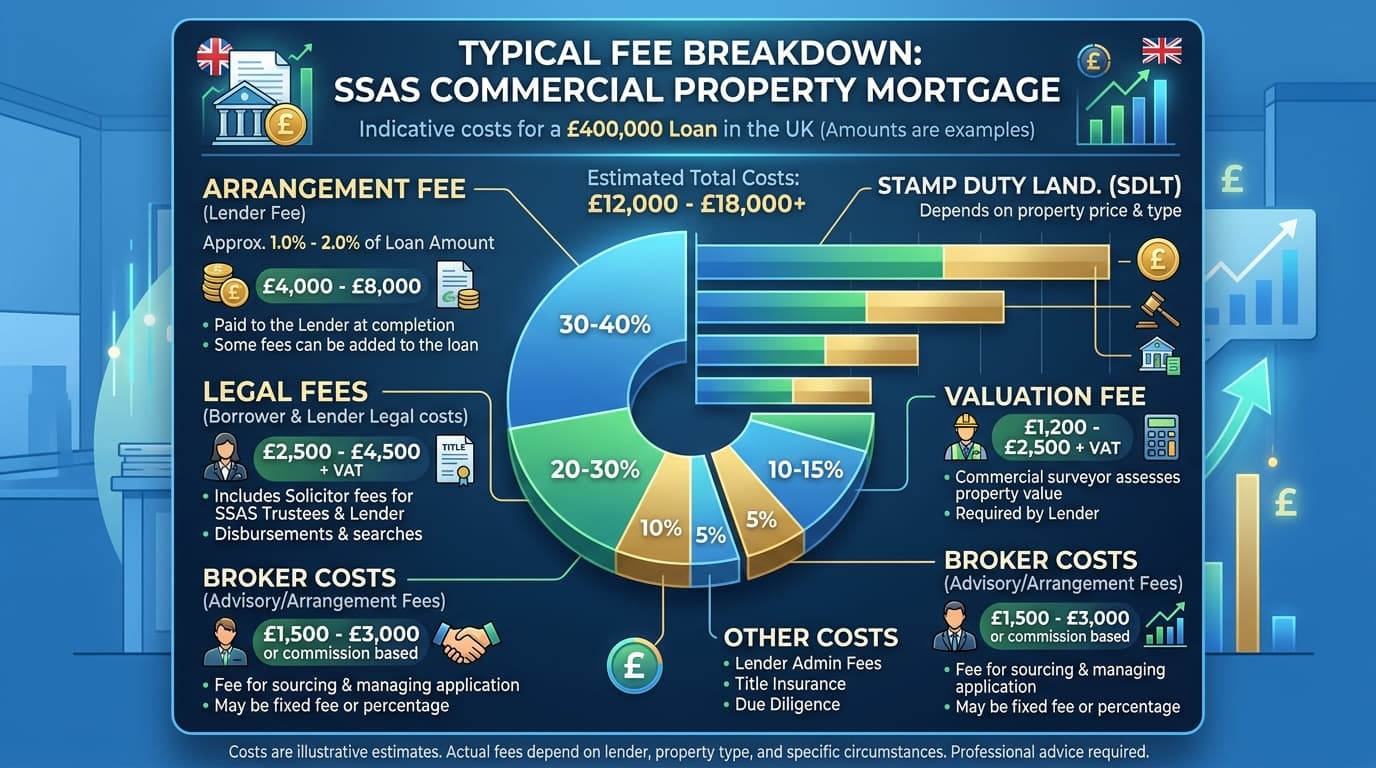

SSAS Arrangement Fees: What You Will Pay and Why

Arrangement fees are a significant upfront cost in any SSAS mortgage. Here is what you are paying for, typical fee levels, and how to evaluate them as part of total cost.

SSAS Lender Criteria Explained: What Lenders Look For

Understanding what SSAS mortgage lenders look for helps you prepare the strongest possible application. Here is a complete breakdown of the key criteria.

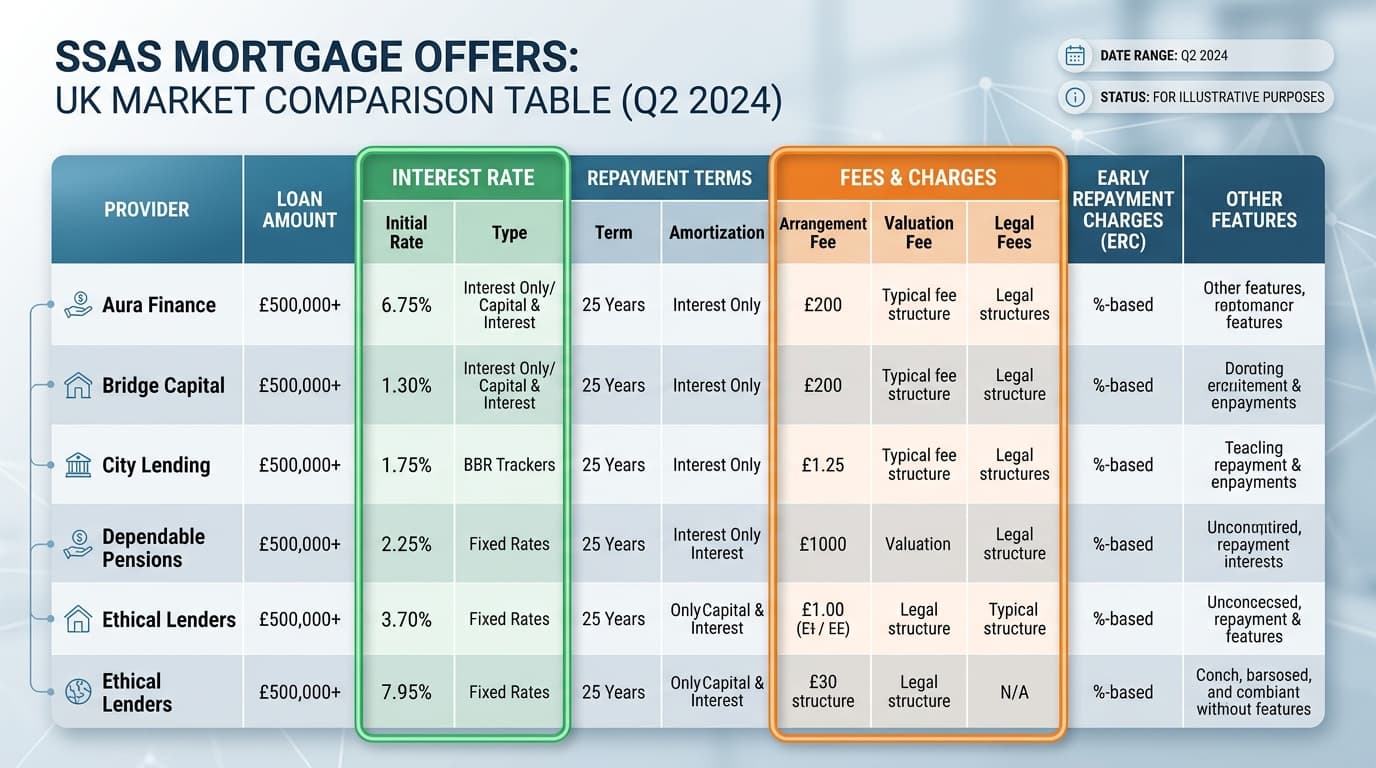

SSAS Rate Comparison Guide: How to Find the Best Deal

Comparing SSAS mortgage rates is more complex than it looks. Here is how to evaluate the true cost of different offers and access the best deals on the market.

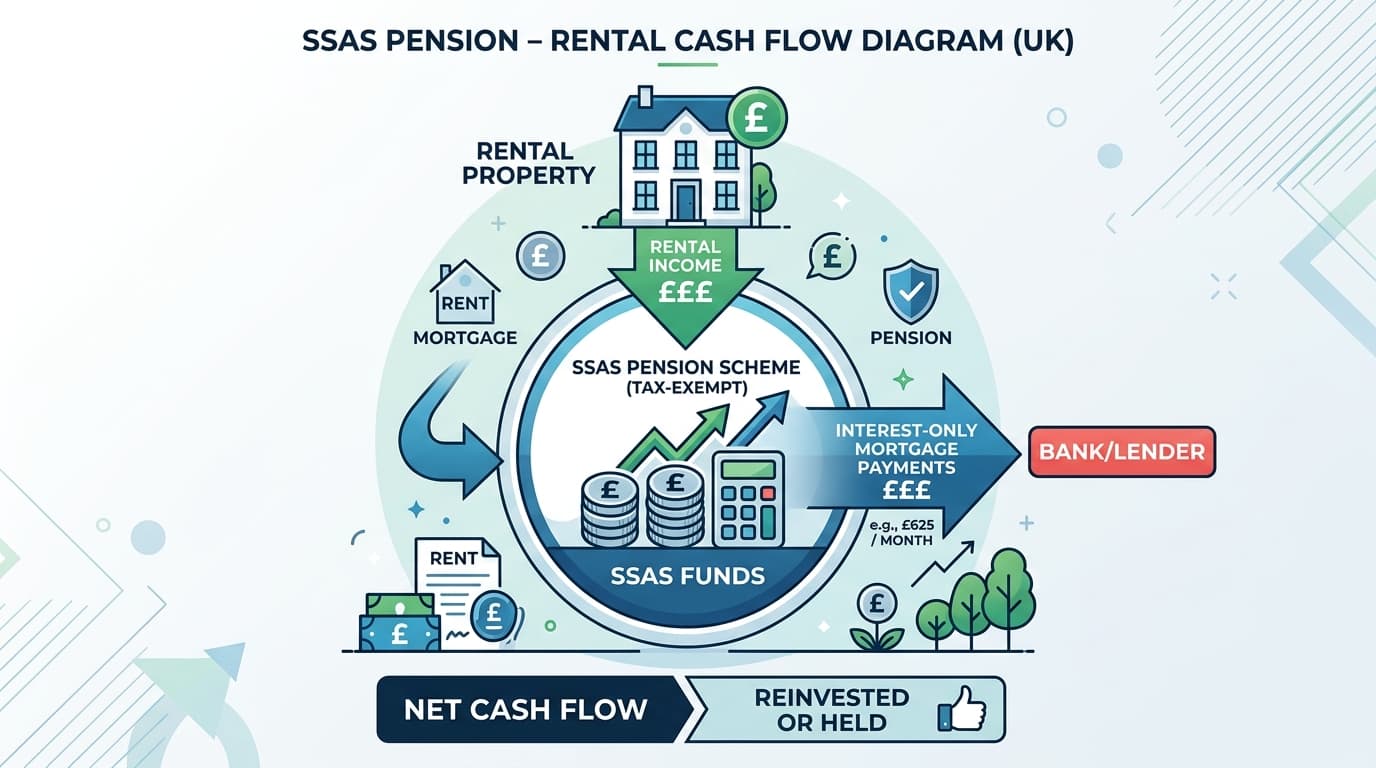

SSAS Interest-Only Mortgages: How They Work for Pension Schemes

Most SSAS property mortgages are structured on an interest-only basis. Here is why, how the cash flows work, and what you need to think about for repayment.

SSAS Development Finance: Funding Property Development Through Your Pension

SSAS development finance is a specialist area that allows pension schemes to participate in commercial property development. Here is what is permitted, what is not, and how to access funding.

SSAS Bridging Finance: When It Works and How to Use It

Bridging finance gives SSAS schemes the speed to secure time-sensitive commercial property deals. Here is how it works, when to use it, and what it costs.

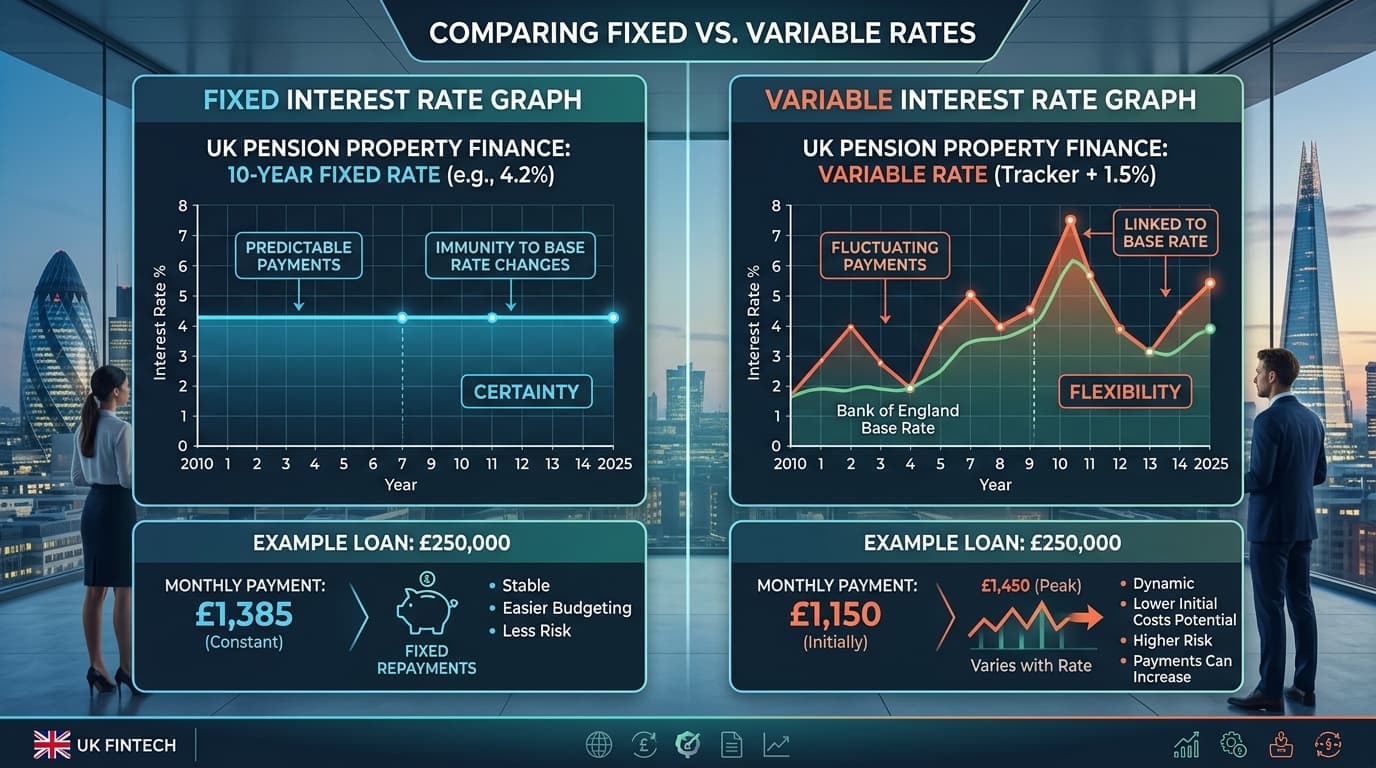

SSAS Fixed vs Variable Rates: Which Is Right for Your Scheme?

Choosing between fixed and variable rates for your SSAS mortgage is a significant financial decision. Here is how to evaluate the trade-offs for your pension scheme.

SSAS Mortgage Rates Explained: What to Expect in 2025

SSAS mortgage rates differ from standard commercial mortgages. Understanding how they are calculated and what drives them is the first step to getting the best deal.

SSAS Sale and Leaseback: How It Works and When to Use It

A SSAS sale and leaseback allows you to sell commercial property to your own pension fund and lease it back. Here is how it works, the tax advantages, and when to use it.

SSAS Connected Party HMRC Rules: The Definitive Guide

HMRC sets detailed rules governing SSAS connected party transactions. This guide covers the legislation, the charges, the reporting requirements, and how to navigate them.

SSAS Connected Party Pitfalls: What Can Go Wrong

SSAS connected party transactions offer significant benefits but come with real risks. Here are the most common pitfalls and how to avoid them.

Benefits of the Connected Party SSAS Lease

Beyond the well-known tax advantages, the SSAS connected party lease delivers a range of strategic business and pension benefits that many business owners overlook.

SSAS Lease Terms for Connected Party Arrangements

A SSAS connected party lease must be drafted to commercial standards. Here are the key terms every SSAS lease needs to include to satisfy HMRC.

SSAS Independent Valuation for Connected Party Transactions

An independent valuation is the cornerstone of SSAS connected party compliance. Here is what type of valuation HMRC requires and how to get it right.

SSAS Market Rent Requirements for Connected Party Leases

Setting the right rent level is critical for SSAS connected party leases. Here is what market rent means, how it is assessed, and how to keep it compliant over time.

SSAS Arms-Length Rules: What They Mean in Practice

The arm's length requirement is the cornerstone of SSAS connected party compliance. Here is what it means in practice and how to ensure your transactions meet the standard.

Renting Commercial Property to Your Company Through Your SSAS

Renting commercial property to your own company via SSAS is one of the most tax-efficient strategies available to UK business owners. Here is how it works in practice.

SSAS Connected Party Transactions: A Complete Guide

SSAS connected party transactions offer powerful tax advantages but come with strict HMRC rules. Understand how to structure a compliant deal that protects your pension.

Choosing the Right Property Type for Your SSAS: A Comprehensive Comparison Guide

Choosing the right commercial property type for your SSAS is one of the most important investment decisions a trustee will make. This comprehensive comparison guide evaluates office, industrial, retail, agricultural, and specialist property types across income, growth, risk, and suitability dimensions.

SSAS Development Land: Investing in Land with Planning Potential Through Your Pension

Development land — or land with planning potential — offers SSAS pension schemes the possibility of transformative returns from planning gain. However, the interaction between development activity and HMRC's investment versus trading rules requires careful management.

SSAS Hotel Property Purchase: Hospitality Assets in Your Pension Scheme

Hotels, guest houses, and serviced accommodation can qualify as SSAS pension investments, but they sit at the intersection of commercial and residential property rules. This guide explains the classification rules, investment case, and financing considerations for hospitality assets.

SSAS Care Home Investment: Healthcare Property in Your Pension Scheme

Care homes and healthcare facilities offer SSAS pension schemes strong income yields and demographic-driven demand growth. This guide explains the investment case, regulatory considerations, and how to structure care home investment within your pension.

SSAS Agricultural Land Investment: Farmland and Pasture in Your Pension

Agricultural land offers SSAS pension schemes a distinctive combination of income, capital growth, and inflation protection. This guide explains which agricultural assets qualify, the rental income potential, and the key considerations for trustees.

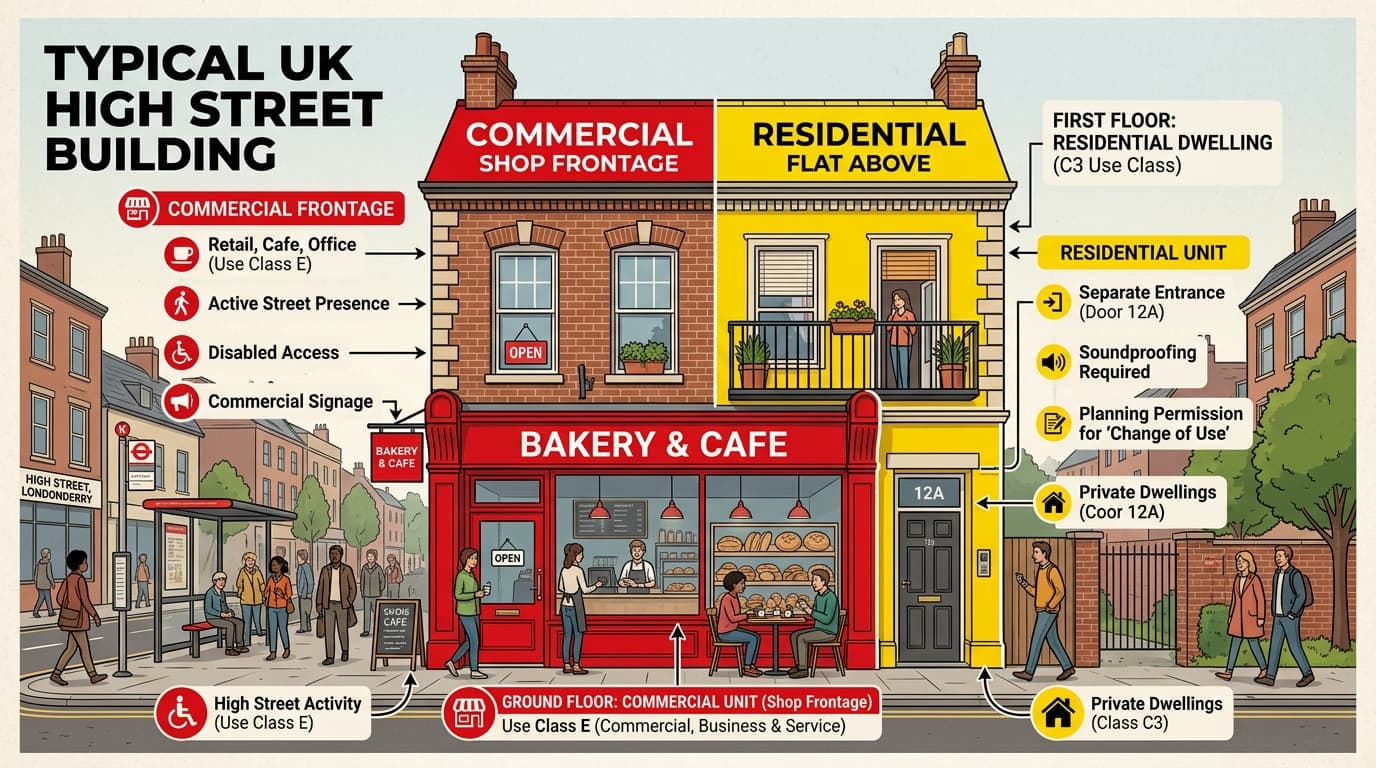

SSAS Mixed-Use Property Investment: Navigating the Commercial and Residential Rules

Mixed-use properties — those containing both commercial and residential elements — are among the most complex for SSAS pension schemes to hold. The residential element triggers HMRC's taxable property rules and can result in severe tax charges. This guide explains the risks and how to navigate them.

SSAS Warehouse Investment: How to Hold Logistics Property in Your Pension

Driven by the e-commerce boom, UK warehouse and logistics property has delivered exceptional returns for investors over the past decade. SSAS pension schemes can access this sector tax-efficiently. This guide explains the investment case and how to get started.

SSAS Retail Premises Guide: Investing in Shops and Retail Property Through Your Pension

Despite well-publicised challenges in the retail sector, retail premises can still be effective SSAS investments when properly selected. This guide covers the investment case, risk considerations, and how to hold retail property efficiently in a pension scheme.

SSAS Industrial Unit Purchase: Warehouses and Light Industrial in Your Pension

Industrial units and warehouses have been among the best-performing commercial property assets in the UK over the past decade. SSAS pension schemes can hold these assets to generate tax-free rental income and CGT-exempt capital growth. This guide explains how.

SSAS Office Property Investment: A Complete Guide for Pension Trustees

Office properties are among the most popular commercial assets for SSAS pension schemes. This guide covers the investment case, HMRC rules, financing considerations, and practical strategies for trustees looking to add office property to their pension portfolio.

SSAS HMRC Reporting Requirements: A Trustee's Complete Reference Guide

SSAS trustees must meet a range of HMRC reporting obligations throughout the year. Missing or inaccurate reports can result in penalties. This guide provides a complete reference covering event reports, Accounting for Tax returns, scheme returns, and annual accounts.

SSAS Tax Planning Strategies: A Comprehensive Guide for Business Owners

SSAS pension schemes offer business owners a uniquely powerful combination of tax advantages. This guide brings together all the key strategies — from tax-free rental income and CGT exemption to employer contributions and estate planning — to create a comprehensive tax planning framework.

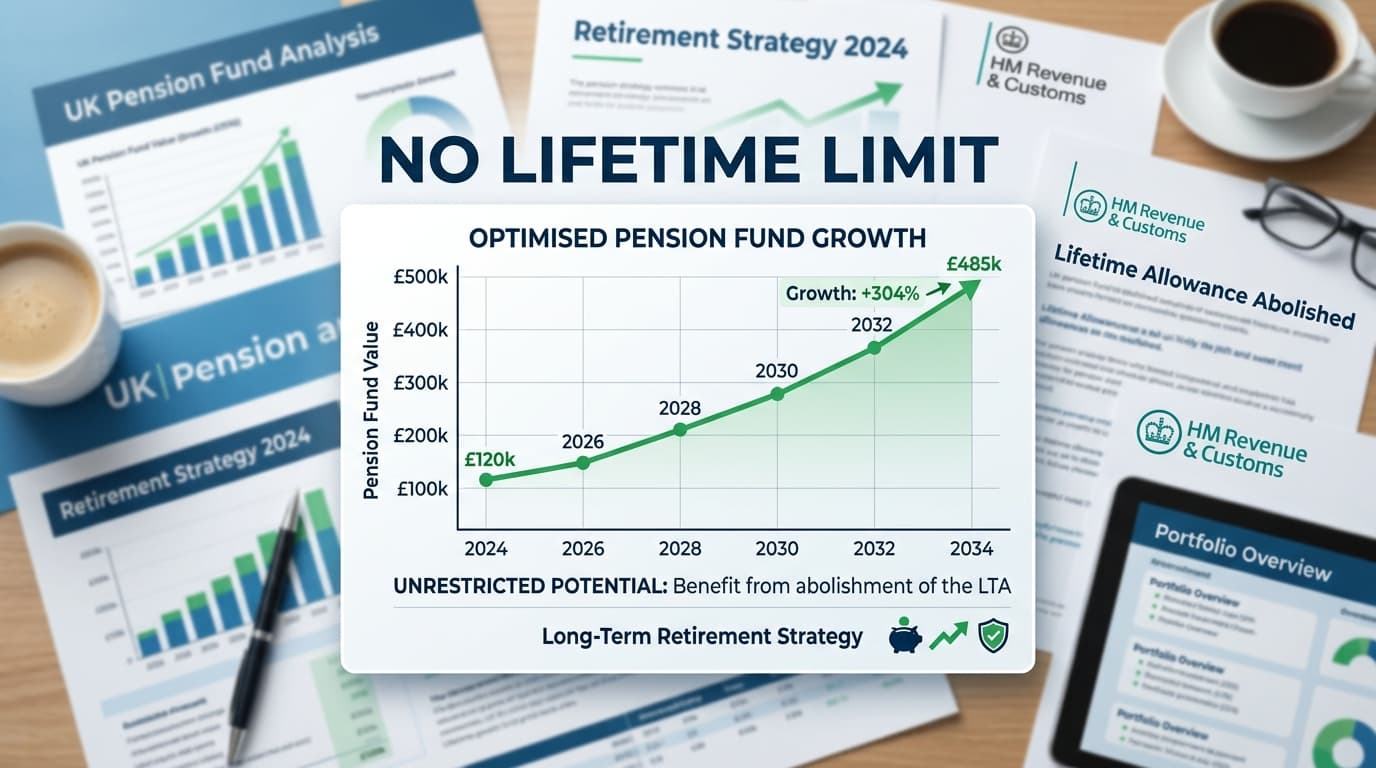

SSAS and the Lifetime Allowance: What the 2023 Changes Mean for Property Investors

The pension lifetime allowance was abolished in April 2024 after decades of limiting how much could be saved in registered pension schemes. This guide explains what changed, what replaced the lifetime allowance, and what it means for SSAS members with significant property-backed pension funds.

SSAS Annual Allowance Guide: Managing Pension Inputs for Maximum Efficiency

The annual allowance is one of the most important concepts in SSAS planning, limiting how much can be contributed to the scheme each year without a tax charge. This guide explains the rules, the carry forward provisions, and practical strategies for maximising pension funding within the limits.

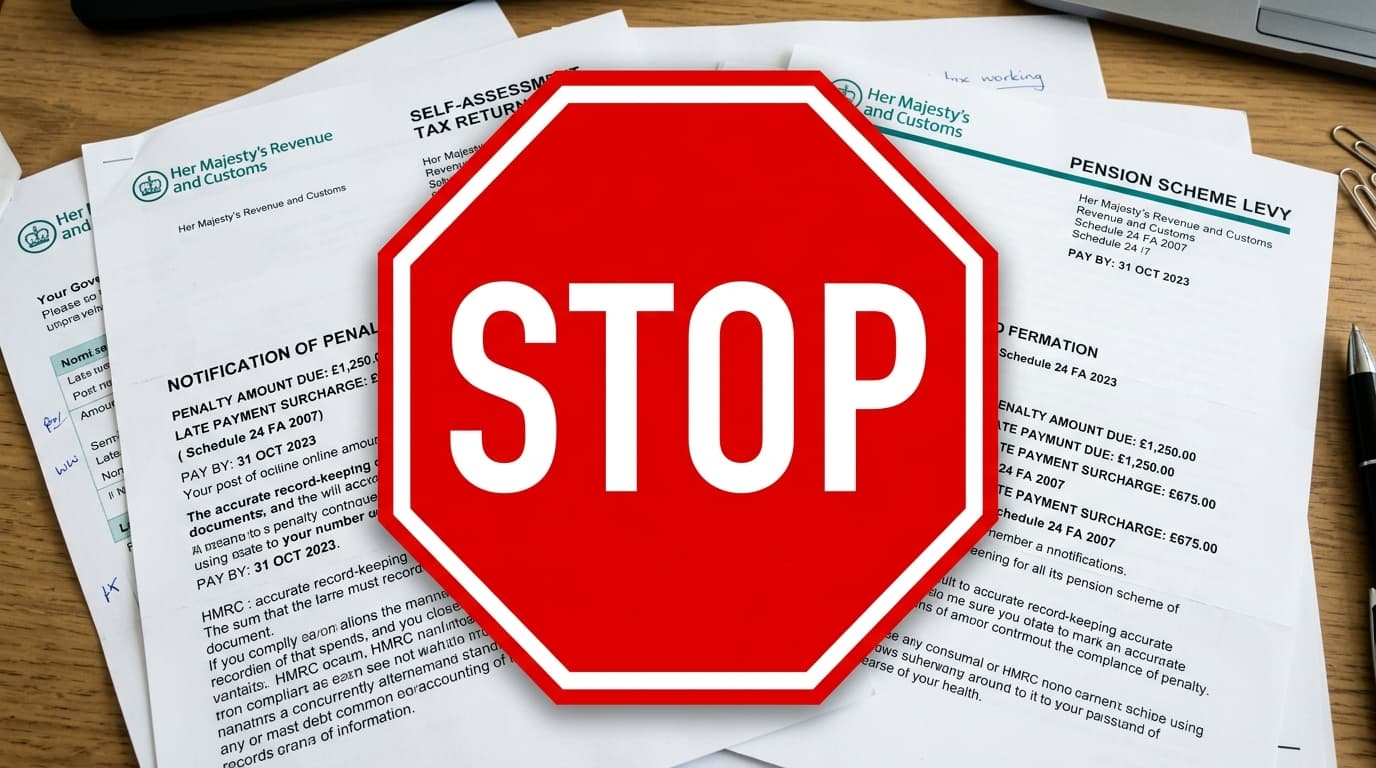

SSAS Scheme Sanction Charges: What They Are and How to Avoid Them

A scheme sanction charge is a tax levied directly on the SSAS pension scheme following certain compliance failures. At up to 40% of the value involved, these charges can be devastating. This guide explains when they apply, how they interact with other penalties, and how to avoid them.

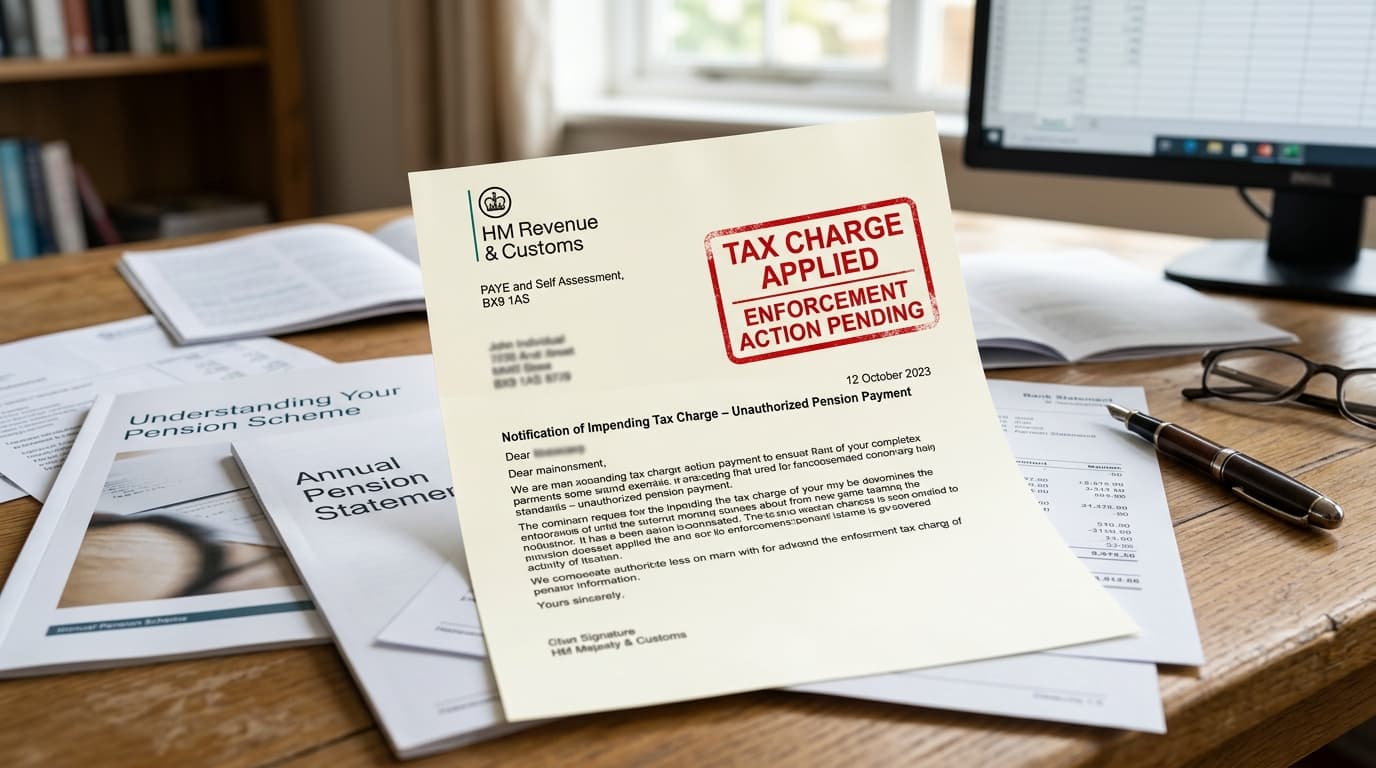

SSAS Unauthorised Payments: Understanding the Risks and How to Avoid Them

An unauthorised payment from a SSAS can trigger tax charges exceeding 55% of the amount involved. This guide explains exactly what constitutes an unauthorised payment, the tax consequences, and the practical steps trustees can take to ensure they never fall foul of the rules.

SSAS HMRC Compliance Guide: What Every Trustee Needs to Know

SSAS trustees have significant legal and tax obligations to HMRC. This guide covers everything trustees need to know about compliance — from scheme registration and annual reporting to investment rules and penalty avoidance.

SSAS Employer Contributions and Tax Relief: Maximising the Pension Funding Advantage

Employer contributions to a SSAS are deductible against corporation tax, making them one of the most efficient ways to fund a commercial property pension strategy. This guide explains the rules, limits, and practical strategies.

SSAS Capital Gains Tax Exemption: Protecting Property Profits Inside Your Pension

When a SSAS pension scheme sells commercial property at a profit, no capital gains tax is payable. This guide explains this powerful exemption, how to qualify, and the strategic implications for long-term property investors.

SSAS Tax-Free Rental Income: How Pension Property Generates Tax-Efficient Returns

One of the most compelling advantages of holding commercial property inside a SSAS pension is the ability to receive rental income completely free of income tax. This guide explains how it works, what HMRC requires, and how to maximise this benefit.

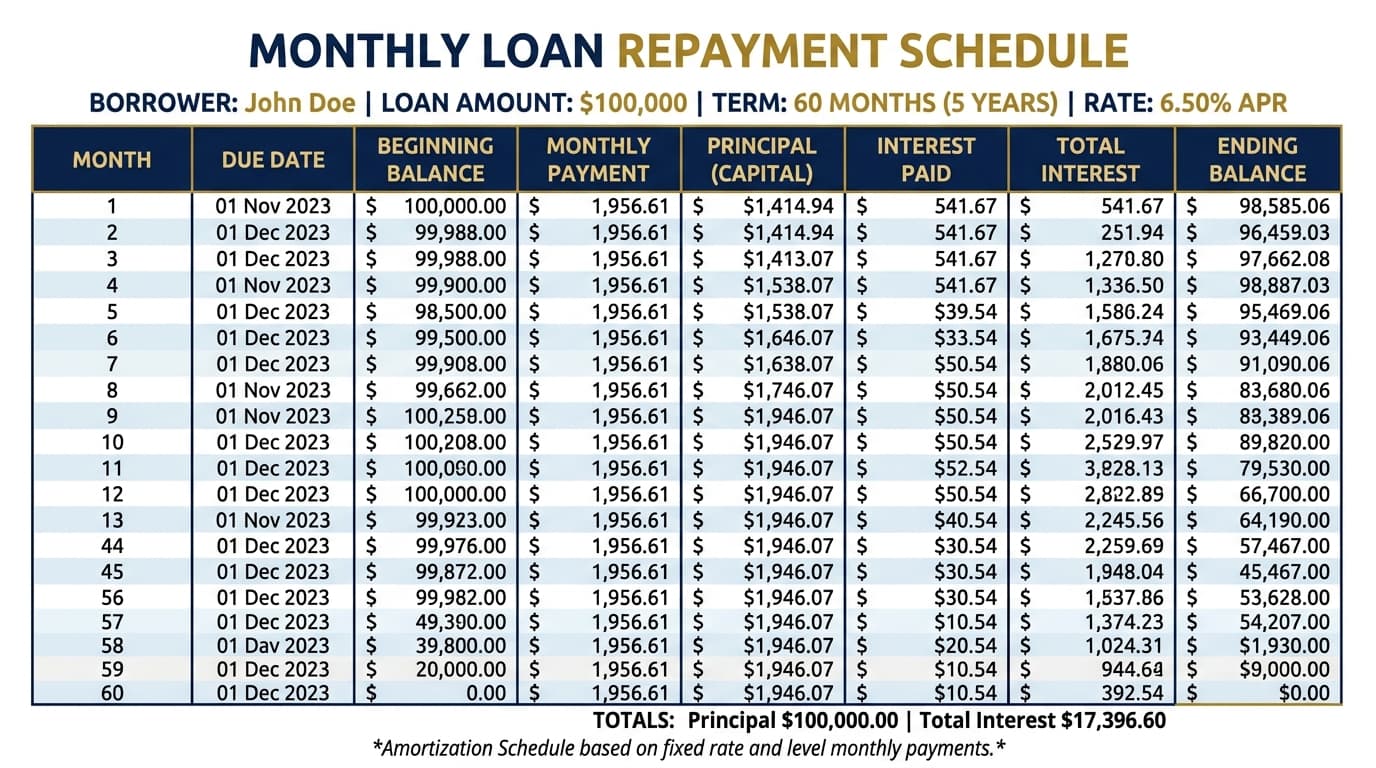

SSAS Loanback Worked Example: A Complete Case Study

See exactly how an SSAS loanback works in practice with this complete numerical case study, from initial assessment through to final repayment.

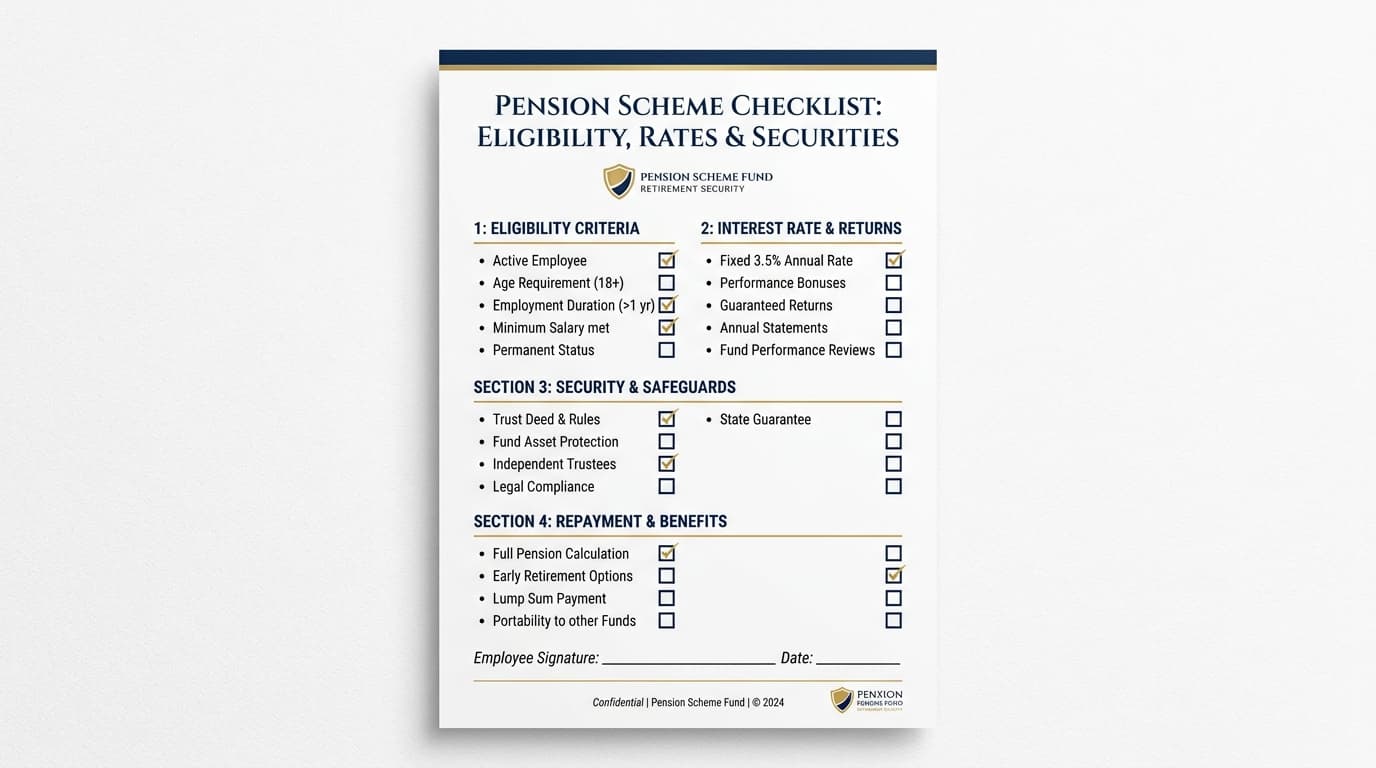

SSAS Loanback Compliance Checklist

Before arranging an SSAS loanback, run through this comprehensive compliance checklist. Every condition must be met to avoid unauthorised payment charges from HMRC.

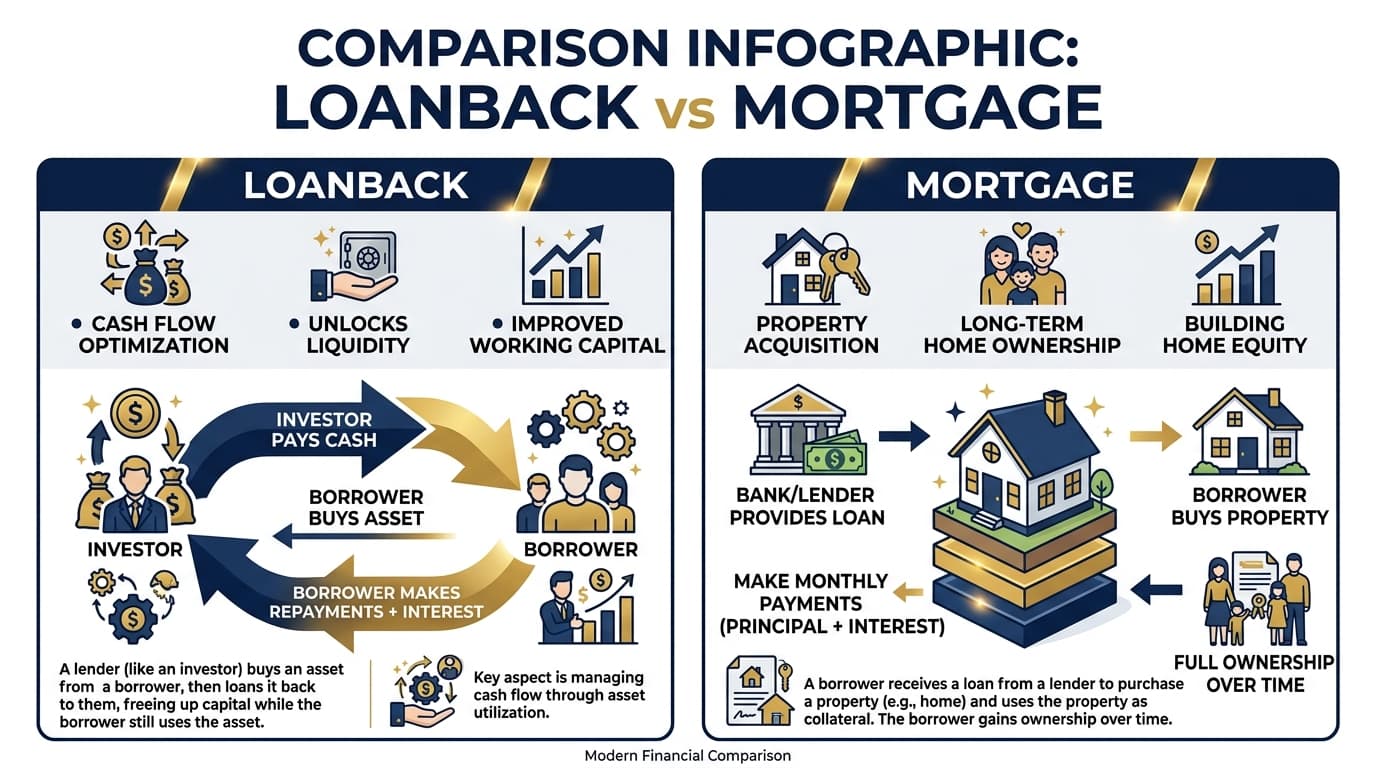

SSAS Loanback vs Mortgage: Which Is Right for Your Business?

Both SSAS loanbacks and SSAS mortgages can fund your business — but they work very differently. This guide helps you understand which is right for your specific situation.

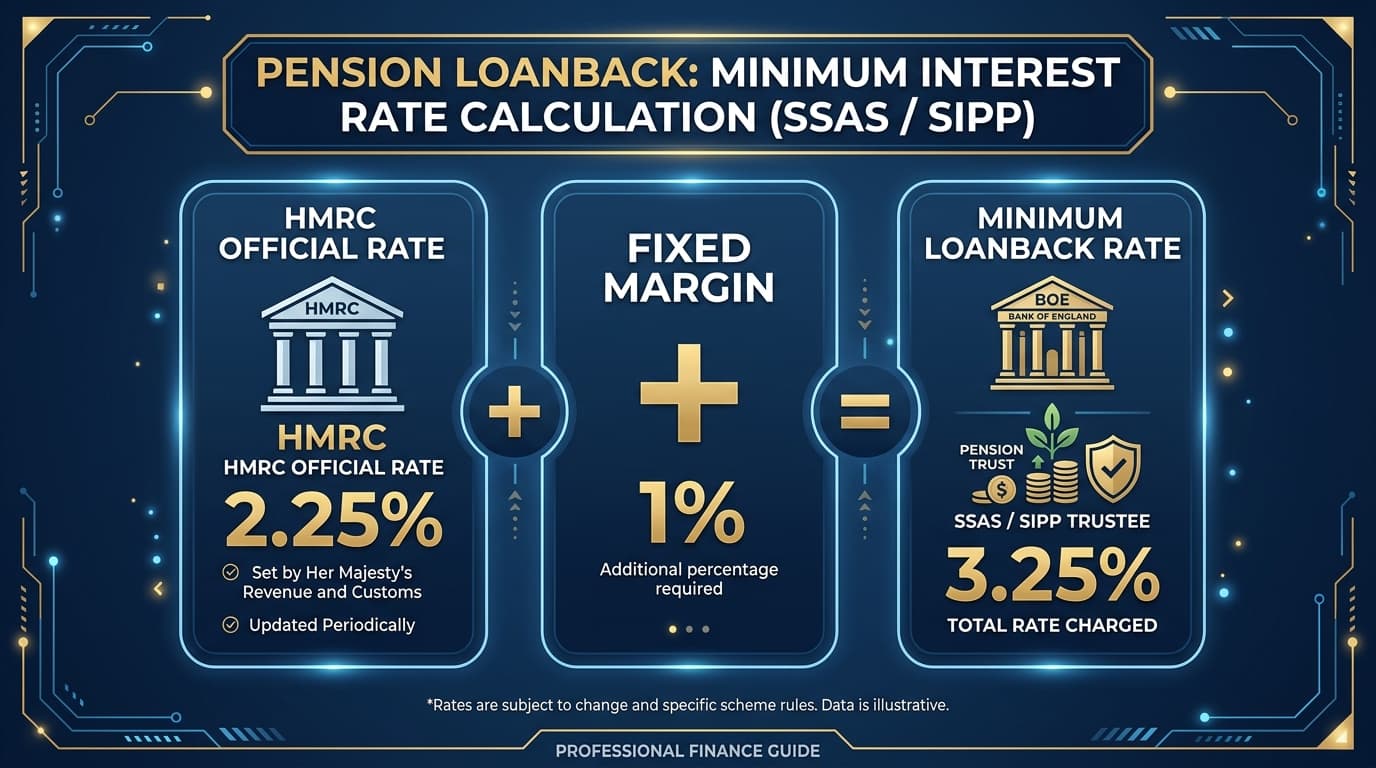

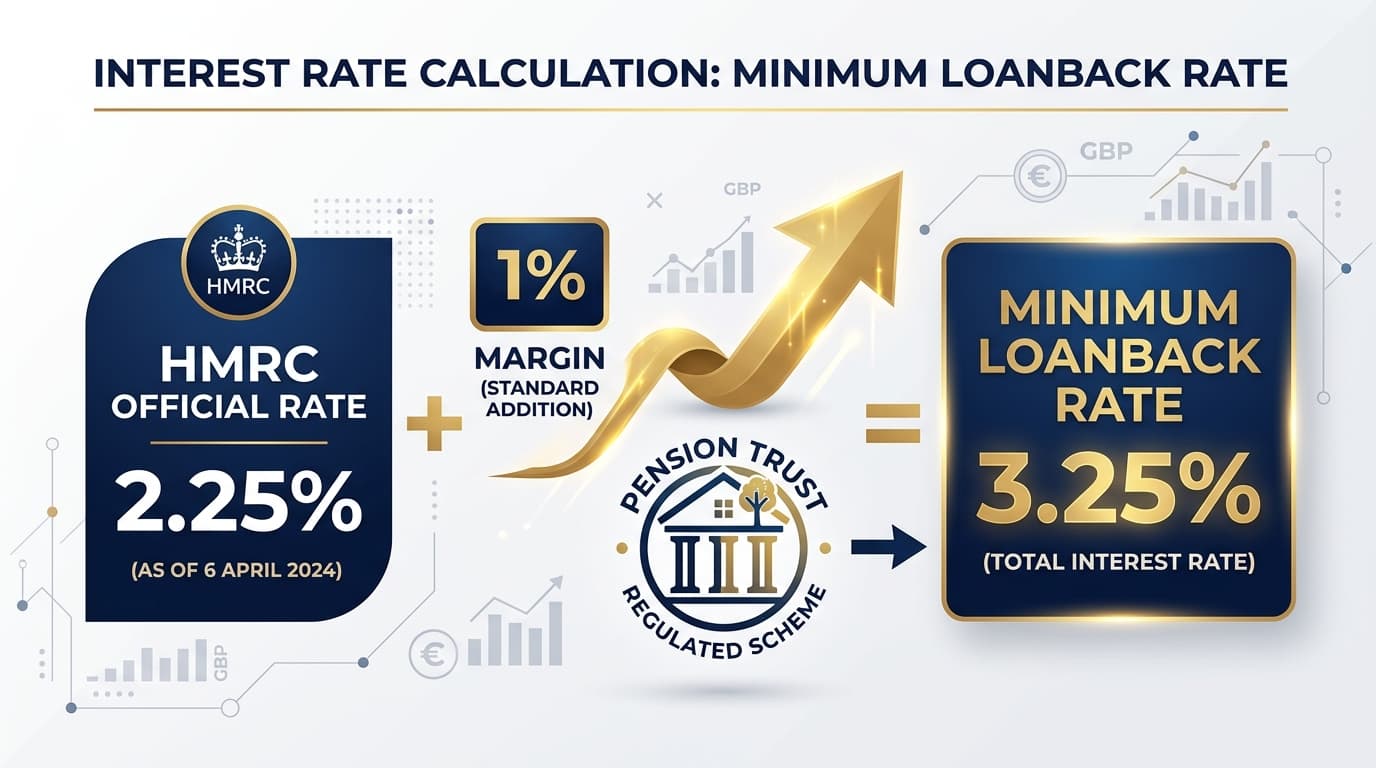

Base Rate Plus 1%: Understanding the SSAS Loanback Minimum Interest Rate

The 'base rate plus 1%' rule is fundamental to SSAS loanback compliance. This guide explains exactly what it means, why it exists, and how to apply it correctly in 2025.

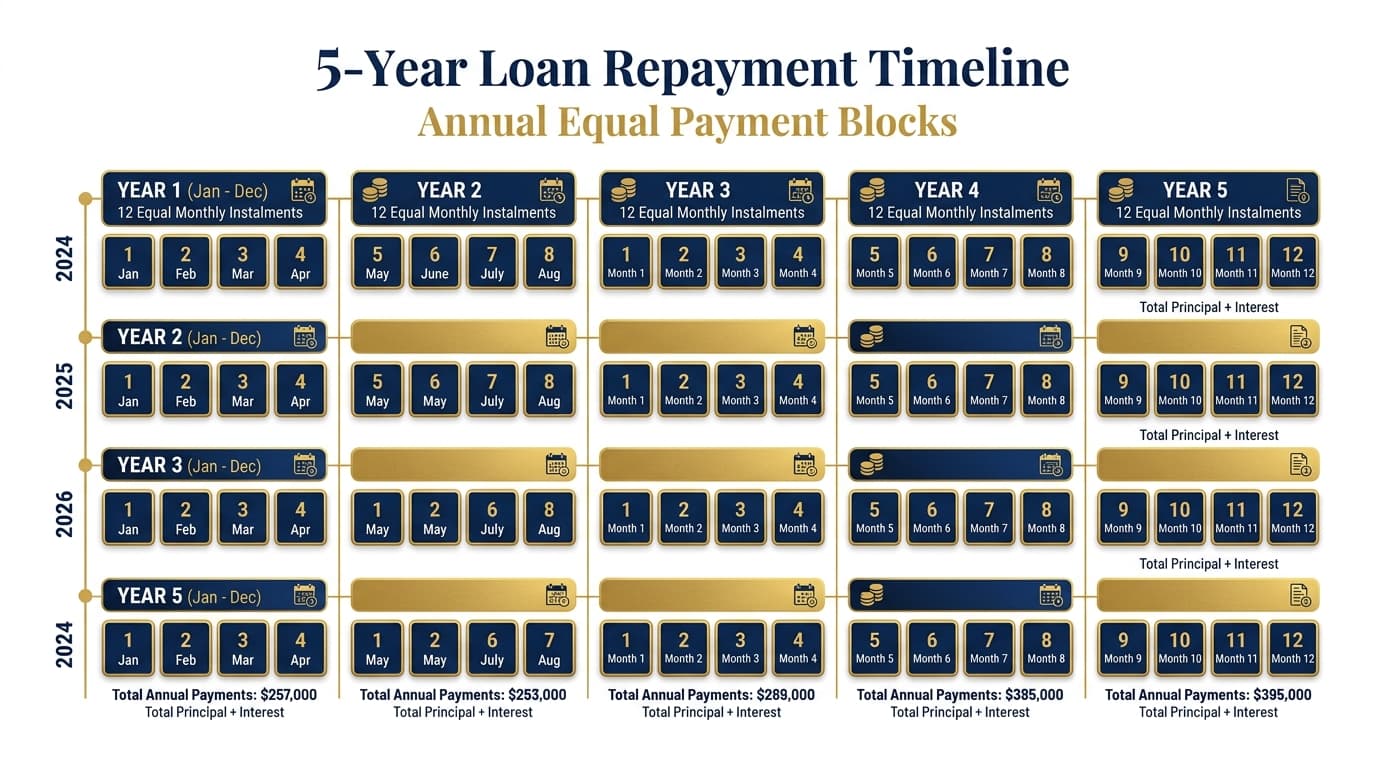

SSAS Loanback Repayment Schedule: Structuring Equal Instalments

A compliant SSAS loanback requires repayment in equal instalments over a maximum of five years. This guide shows you exactly how to structure and document the repayment schedule.

Permitted Uses of SSAS Loanback Funds

SSAS loanback funds must be used for legitimate business purposes by the sponsoring employer. This guide explains what HMRC permits, what is prohibited, and how to document the use correctly.

SSAS Loanback Security Requirements

Every SSAS loanback must be secured by a first charge over employer assets equal to at least the loan value. This guide explains what qualifies as acceptable security and how to arrange it.

SSAS Loanback Interest Rate Rules: Base Rate Plus 1%

SSAS loanbacks must charge interest at no less than base rate plus 1%. This guide explains why, what the current minimum rate is, and how to structure interest payments correctly.

The SSAS 5-Year Repayment Rule Explained

The 5-year repayment rule is one of the most critical SSAS loanback requirements. Understanding it — and what happens if you can't meet it — is essential for every SSAS trustee.

SSAS Loanback Rules Explained

The SSAS loanback is one of the most powerful tools available to small business owners — but HMRC rules are strict. This guide explains every requirement you must meet to stay compliant.

SSAS Borrowing vs. Cash Purchase: Which Is Better for Your Pension Scheme?

When your SSAS has sufficient cash to buy a property outright, should you still borrow? The answer depends on your scheme's specific circumstances, growth objectives, and risk appetite.

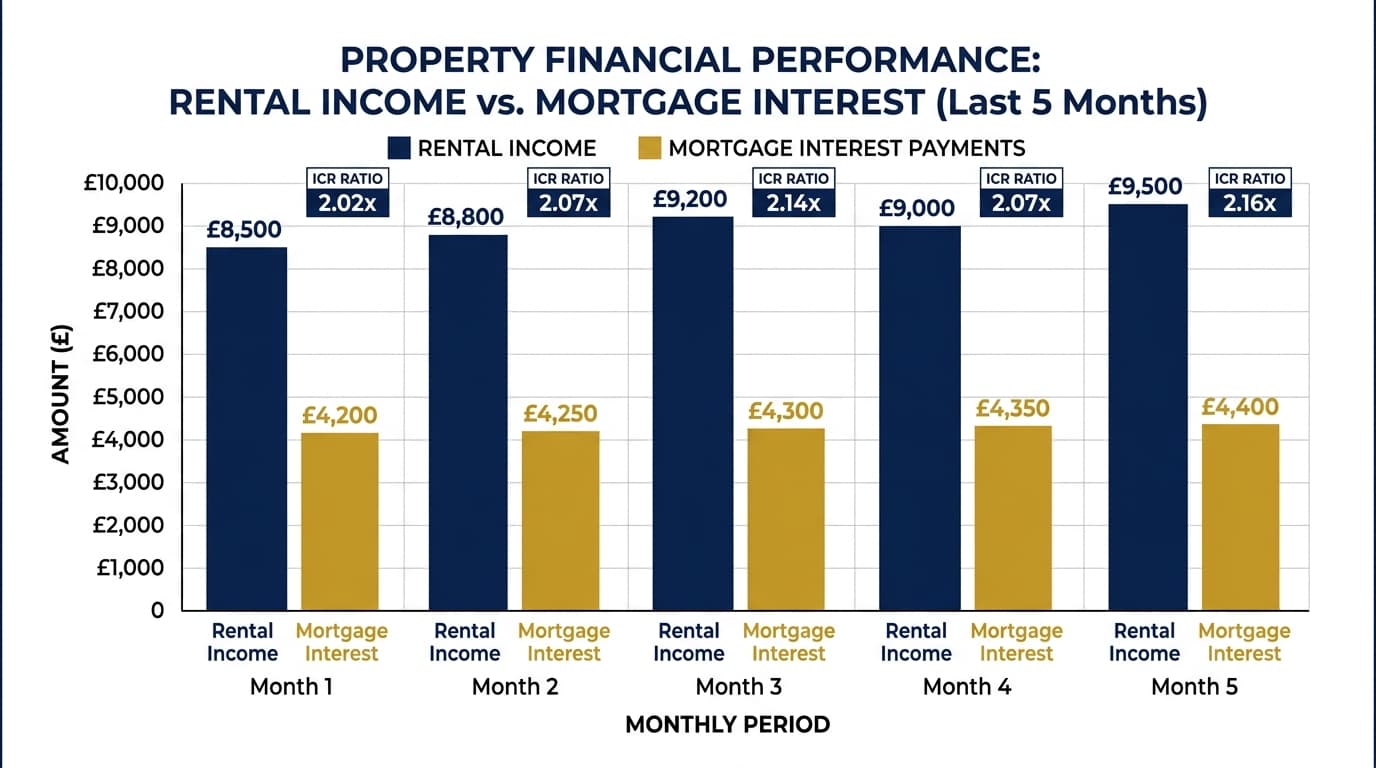

SSAS Debt Service Coverage Ratios Explained

The interest coverage ratio is a critical affordability test for SSAS mortgages. This guide explains how lenders calculate it, what thresholds they apply, and how to assess your target property.

Bridging to Term Loan: Using Bridging Finance in an SSAS

Bridging finance can allow your SSAS to acquire properties faster than a standard mortgage permits. Here's how the bridging-to-term-loan strategy works for pension schemes.

SSAS Refinancing Guide: When and How to Remortgage Your Pension Property

Refinancing your SSAS property can reduce costs, release equity for new investments, or extend your loan term. This guide explains when refinancing makes sense and how to execute it.

Pooling Resources Across Multiple SSAS Members

One of the most powerful advantages of an SSAS over an individual SIPP is the ability to pool resources across multiple members. Here's how it works and how to structure it effectively.

SSAS Borrowing Power Calculation: A Complete Guide

Calculating your SSAS borrowing power requires combining the HMRC net asset value test with lender-specific underwriting criteria. This guide walks you through the full calculation with worked examples.

SSAS Deposit Requirements: How Much Cash Does Your Scheme Need?

How much cash does your SSAS actually need to put down? This guide covers typical deposit requirements, acceptable funding sources, and strategies when your scheme is short on liquidity.

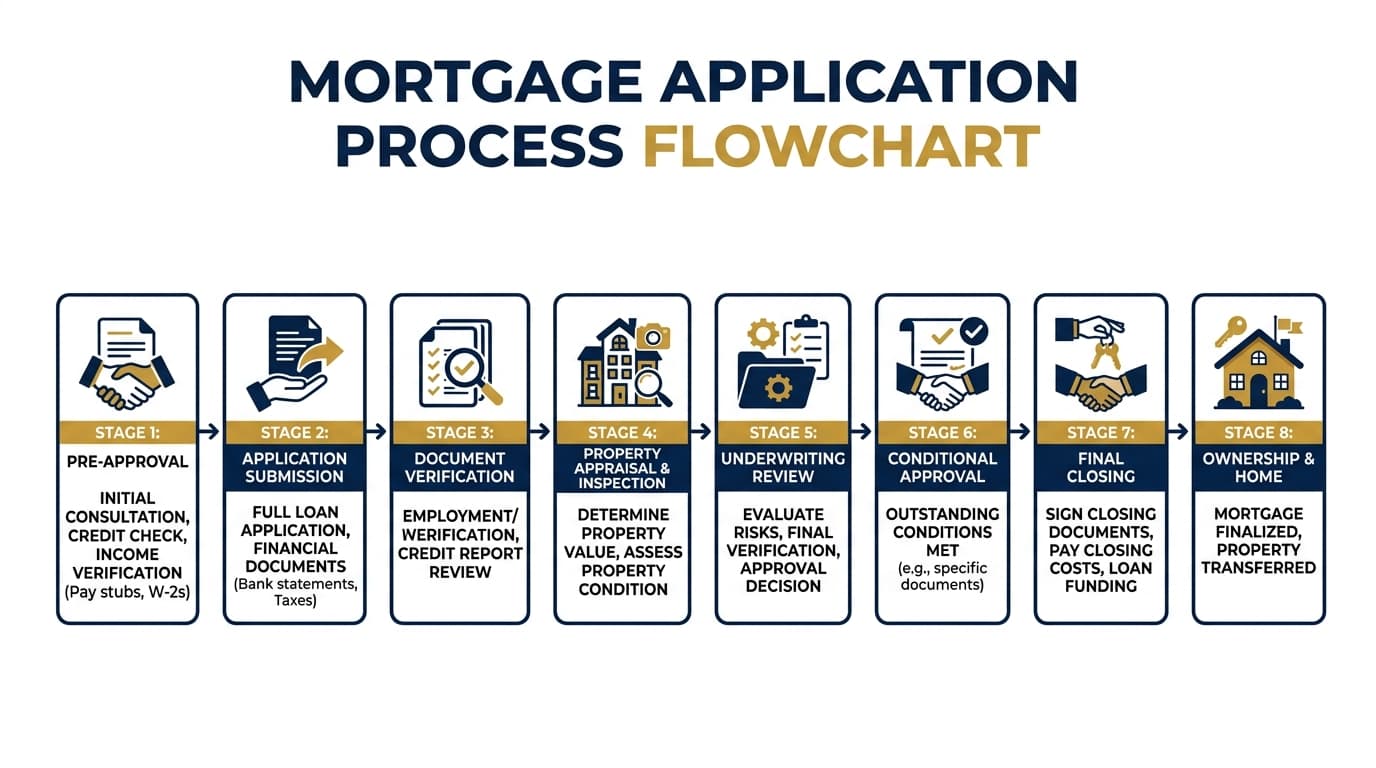

The SSAS Mortgage Application Process: A Step-by-Step Guide

Applying for an SSAS mortgage is more involved than a standard commercial mortgage. This step-by-step guide explains every stage of the process, from initial enquiry to completion.

How Much Can an SSAS Borrow?

Calculating your SSAS maximum borrowing isn't straightforward. This guide breaks down the HMRC rules, lender criteria, and real-world examples to show exactly how much your scheme can access.

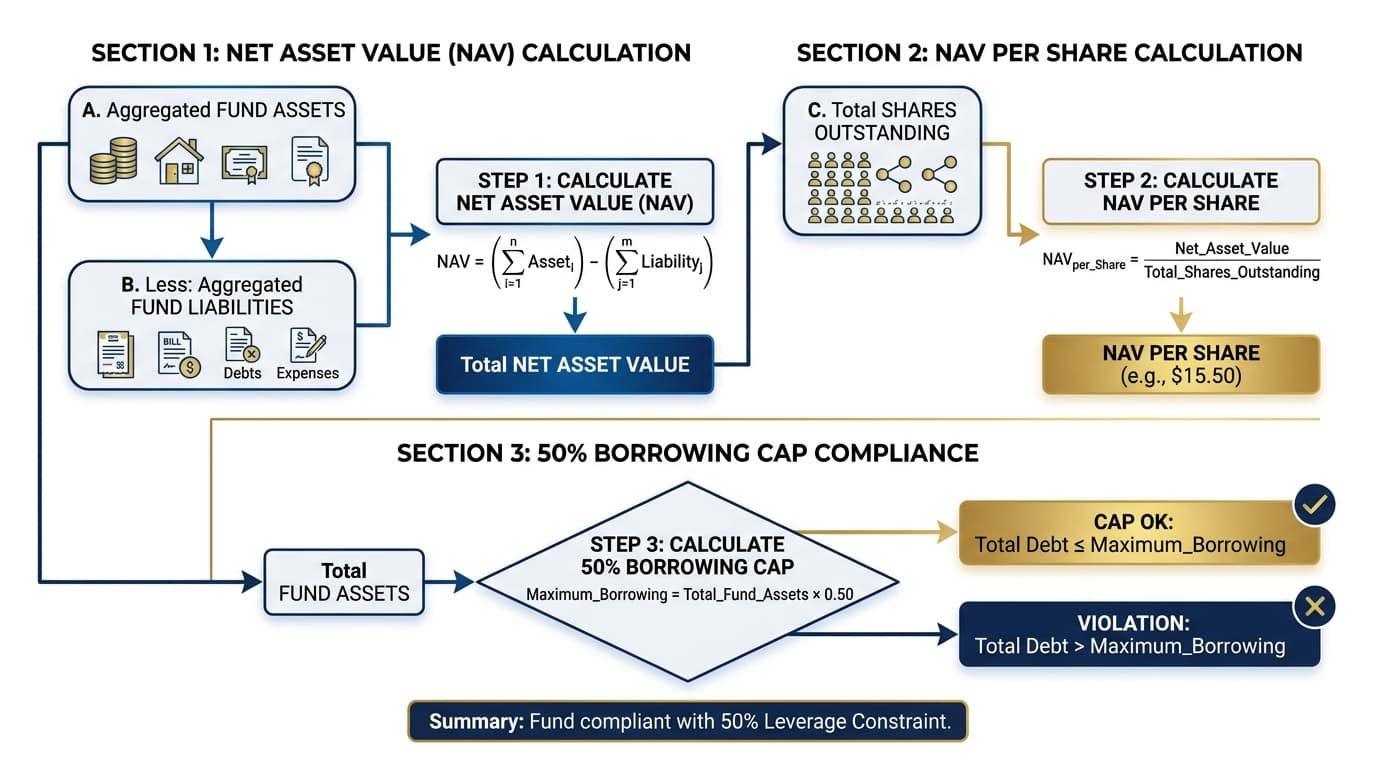

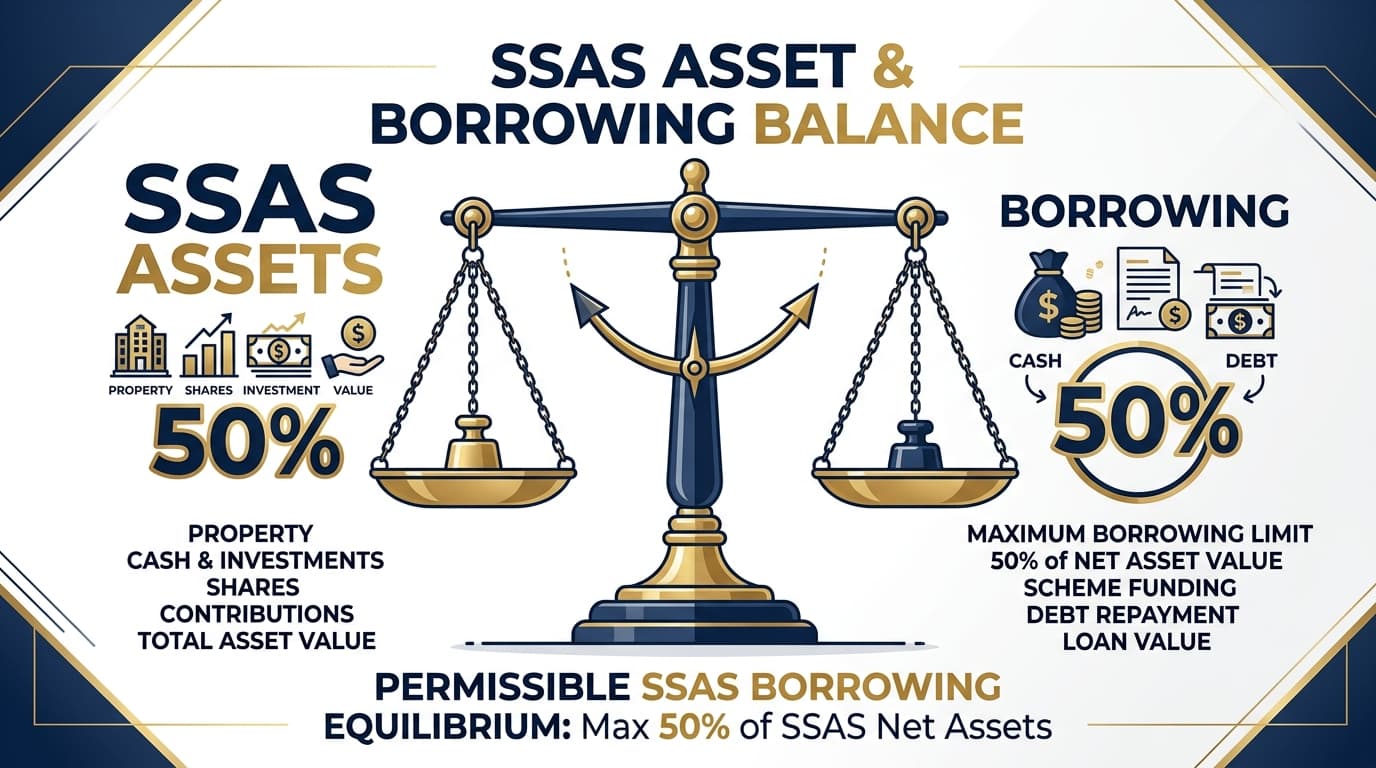

The SSAS 50% LTV Cap Explained

The 50% LTV cap is one of the most misunderstood rules in SSAS property finance. Here's exactly how it works, how it's calculated, and how to structure deals within it.

Post-Completion SSAS Property Management: Your Ongoing Obligations

Completing an SSAS commercial property purchase is not the end of the process — it is the beginning of an ongoing management responsibility. This guide covers everything trustees need to know about managing a commercial property within an SSAS from completion day onwards.

The SSAS Trustee Approval Process for Property Purchases

Before an SSAS can exchange contracts on a commercial property, the trustees — including the pensioneer trustee — must formally approve the transaction. Understanding what they review and what documentation is required prevents delays and ensures governance compliance.

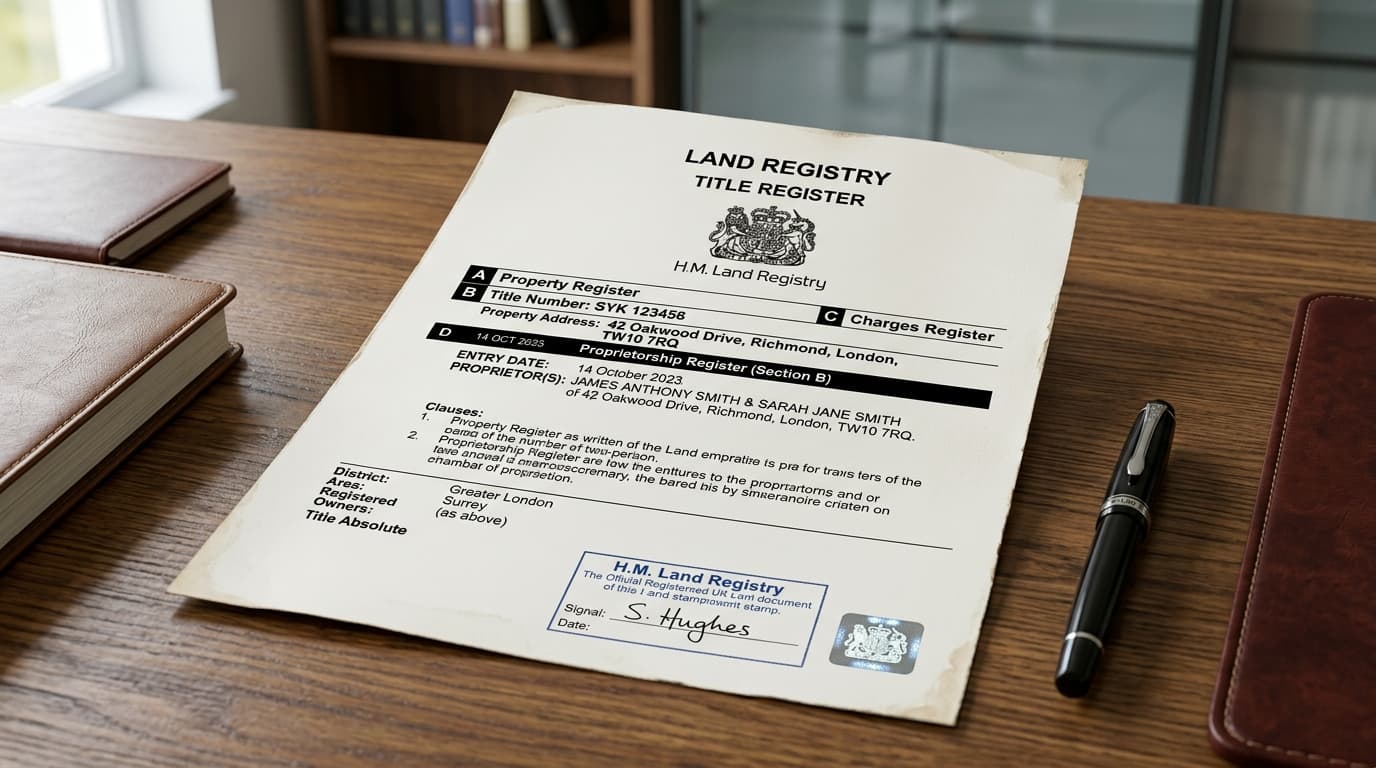

SSAS Title Registration: Registering Your Pension Scheme as Property Owner

Registering an SSAS-owned commercial property at HM Land Registry in the correct trustee names is a critical post-completion step that protects the scheme's ownership. This guide explains the registration process, what can go wrong, and how to keep the register up to date.

RICS Valuations for SSAS Property Purchases: A Trustee's Guide

The RICS Red Book valuation is a cornerstone of the SSAS property purchase process. This guide explains what the valuation involves, how to select and instruct the right surveyor, and what to do if the valuation result creates complications for your transaction.

SSAS Property Due Diligence: What Trustees Must Investigate Before Buying

Trustees of an SSAS owe a duty to conduct proper due diligence before committing to any investment. For commercial property purchases, this means investigating legal title, physical condition, financial performance, tenant covenant strength, and HMRC compliance — all before exchanging contracts.

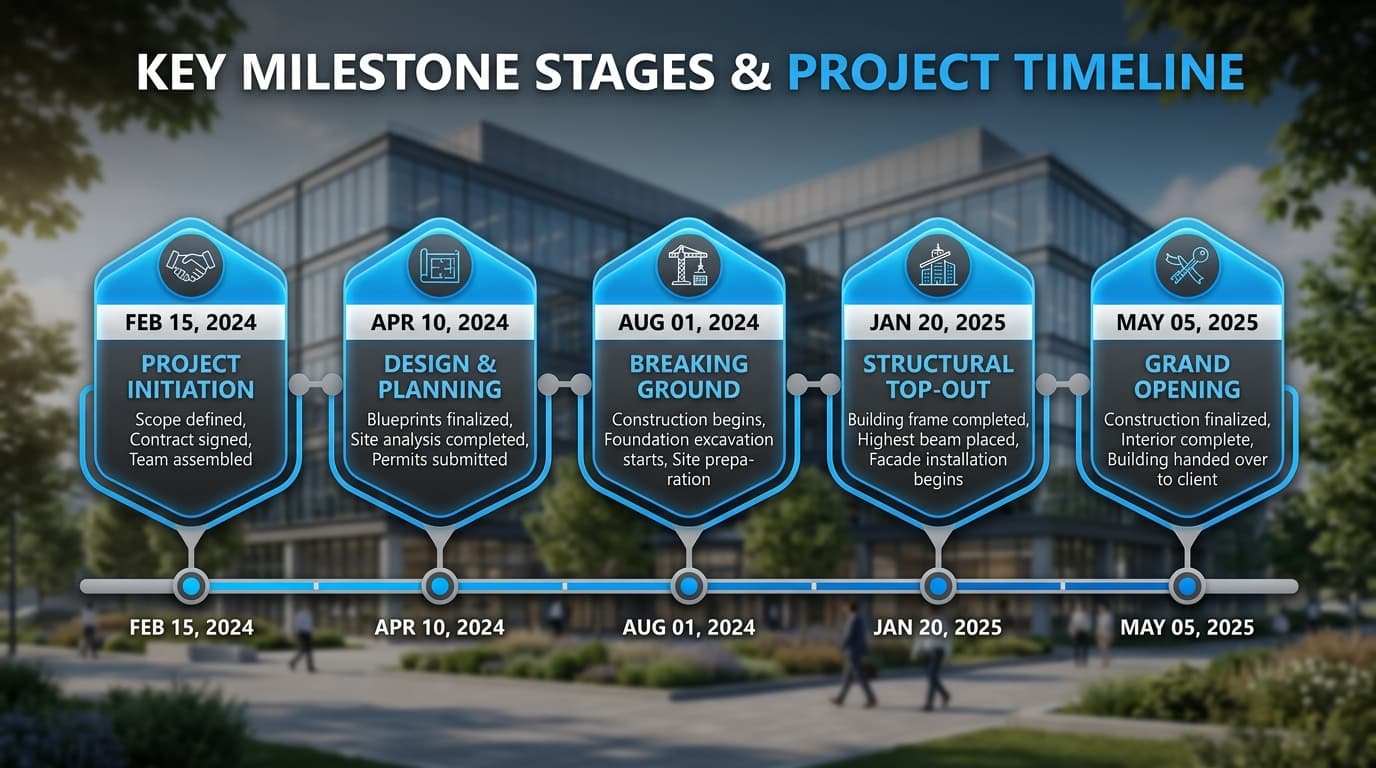

SSAS Property Completion Timeline: How Long Does It Take?

SSAS property purchases take longer than standard commercial transactions due to the additional governance, valuation, and mortgage underwriting steps involved. Understanding the typical timeline helps trustees manage expectations and plan proactively.

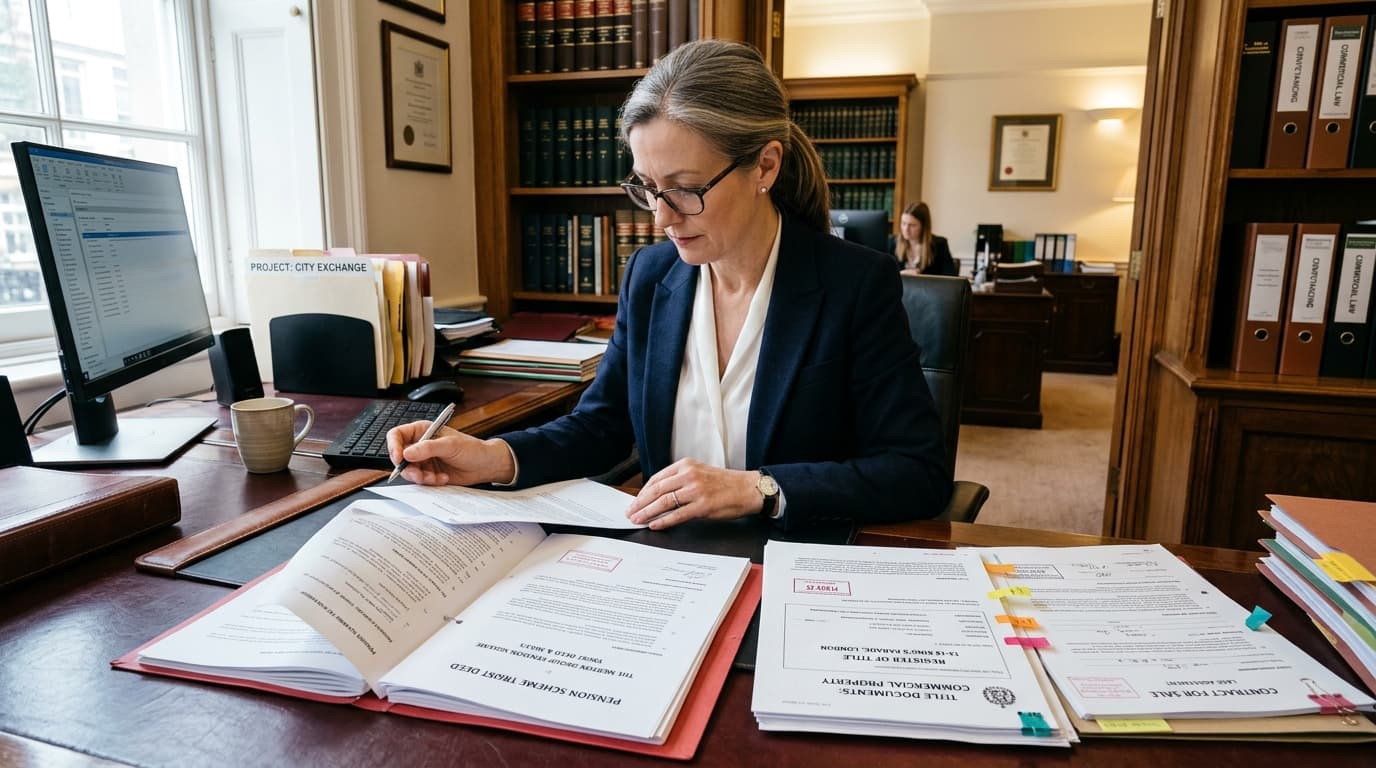

The Role of the Solicitor in an SSAS Property Purchase

The solicitor acting for SSAS trustees in a commercial property purchase plays a central role in ensuring the transaction is legally sound, HMRC-compliant, and completed on time. Understanding their role helps trustees manage the process more effectively.

SSAS Property Valuation Requirements: What You Need to Know

An independent RICS valuation is not just good practice for SSAS property transactions — it is an HMRC requirement. Understanding when valuations are needed, what they cover, and how to commission one correctly is essential for every SSAS trustee.

SSAS Property Purchase Step by Step: From Offer to Completion

Purchasing commercial property through an SSAS involves more parties and more steps than a standard property transaction. Understanding each stage — from trustee approval to HMRC compliance checks — helps you manage timelines and avoid the delays that can derail deals.

Buying Commercial Property Through an SSAS: The Complete Guide

Purchasing commercial property through an SSAS is one of the most powerful retirement planning strategies available to UK business owners. This guide covers everything you need to know — from eligible property types to completing the transaction and managing the asset post-purchase.

SSAS Investment Powers: What Can Your Pension Scheme Actually Hold?

The SSAS's wide investment powers are one of its most compelling features. But the flexibility comes with important limits: certain investments are expressly prohibited, and breaching these rules triggers severe tax consequences. This guide maps out exactly what your SSAS can and cannot hold.

SSAS Pension Transfers: Consolidating Your Pensions for Property Investment

Transferring existing pension funds into an SSAS is one of the fastest ways to build the scheme's investment capacity. Understanding the transfer process, the risks of transferring defined benefit pensions, and the rules around transfer-in-specie can help you consolidate your retirement savings efficiently.

Winding Up an SSAS: What Trustees Need to Know

Winding up an SSAS is a significant undertaking that requires careful planning, trustee consensus, and proper HMRC notification. Whether triggered by retirement, death, or a decision to transfer assets elsewhere, understanding the process protects members and avoids unnecessary tax charges.

SSAS Scheme Administration: Who Does What and Why It Matters

Effective SSAS administration is the backbone of a compliant, well-run pension scheme. Understanding who is responsible for what — and what the annual obligations are — protects the scheme's tax status and gives members confidence in their retirement planning.

SSAS Employer Contributions: Maximising Tax Relief for Your Business

Employer contributions to an SSAS are one of the most tax-efficient ways for a company to extract value for its directors while reducing its corporation tax bill. Understanding the rules around contribution levels, timing, and carry forward can dramatically accelerate your pension fund.

SSAS Member Benefits: How Directors Draw Retirement Income

Understanding how you will eventually draw benefits from your SSAS is as important as understanding how to build it. This guide covers pension commencement lump sums, flexi-access drawdown, annuity options, and the powerful death benefit planning opportunities that SSASs offer.

SSAS Trustee Responsibilities: What Every Trustee Needs to Know

Acting as an SSAS trustee is a significant legal and fiduciary responsibility. Trustees must act in the best interests of members, ensure regulatory compliance, and exercise care and diligence in all investment decisions. Here is what you need to know.

Setting Up an SSAS: A Step-by-Step Guide for Business Owners

Setting up an SSAS involves legal documentation, HMRC registration, and the appointment of a pensioneer trustee. This guide walks you through every stage of the process, from initial planning to making your first investment.

SSAS vs SIPP for Property Investment: Which Is Right for You?

Both SSAS and SIPP pensions can hold commercial property tax-efficiently, but they differ fundamentally in structure, flexibility, and what they can do for your business. Here is how to decide which is right for your circumstances.

What Is an SSAS Pension? A Complete Guide for Business Owners

A Small Self-Administered Scheme (SSAS) is a powerful occupational pension arrangement that gives business owners and company directors unparalleled control over their retirement savings — including the ability to purchase commercial property and lend money back to the sponsoring employer.