SSAS Property Purchase Step by Step: From Offer to Completion

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

Why SSAS Property Purchases Take Longer

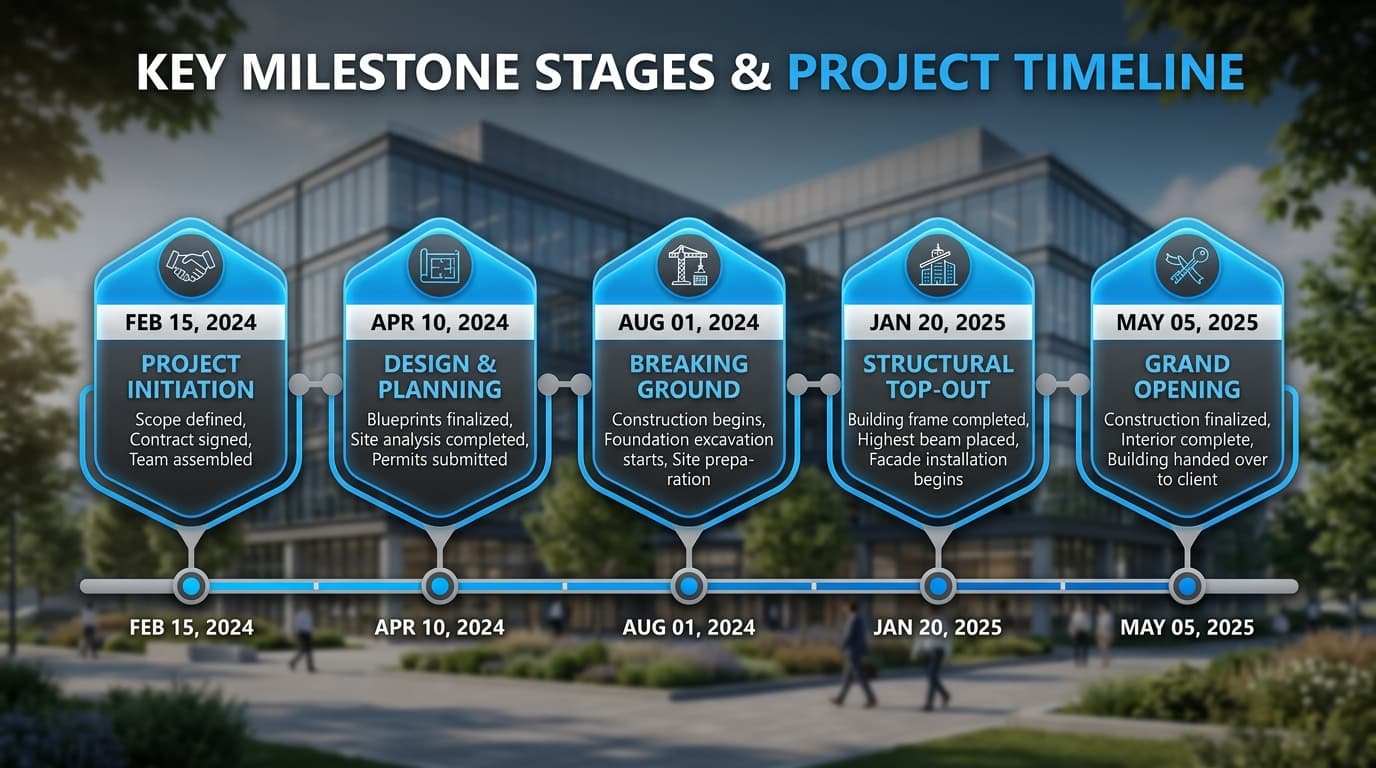

A commercial property purchase through an SSAS takes longer than a standard commercial purchase, typically 10-16 weeks from offer acceptance to legal completion. The additional time is driven by:

- The requirement for pensioneer trustee approval at key stages

- An independent RICS valuation that must precede exchange of contracts

- Specialist SSAS mortgage underwriting and legal requirements

- Multiple parties (member-trustees, pensioneer trustee, solicitor, lender, lender's solicitor) who must each be satisfied before proceeding

In our experience, the deals that complete most smoothly are those where the trustees understand the process in advance and have proactively assembled their professional team before making an offer. A solicitor who has never acted for an SSAS trustee, or a lender encountering a pension trust borrower for the first time, will slow the process considerably.

Stage 1: Trustee Approval to Proceed

Before making any offer, the trustees should convene formally (even informally by email, with minutes recorded) to agree that:

- The property fits within the scheme's investment policy and powers

- The proposed purchase price is consistent with an independent valuation

- The scheme has (or will have) sufficient funds to complete, including any borrowing

- The pensioneer trustee has been informed and has no preliminary concerns

This upfront alignment avoids the embarrassing situation of an offer being accepted and then failing to progress because the trustees have not properly considered the purchase.

Stage 2: Making the Offer

Once the trustees are aligned, an offer can be made. The offer should be subject to RICS valuation and SSAS trustee approval — standard conditions for a pension scheme purchaser. Many vendors and their agents will be familiar with SSAS purchasers and will accept these conditions without difficulty.

Identify yourself clearly as purchasing as SSAS trustees. This helps the vendor's solicitors prepare the right form of documentation from the outset. For more on the solicitor's role, see our guide on the role of the solicitor in an SSAS purchase.

Stage 3: Instructing the Professional Team

Immediately upon offer acceptance, instruct:

- SSAS solicitor: Must be experienced in pension trust conveyancing. They will handle the legal due diligence, title investigation, and completion

- RICS surveyor: To conduct an independent valuation of the property

- Mortgage broker / lender: If borrowing is required, applications should be submitted immediately — SSAS mortgage underwriting takes time

Delays in instructing professionals are the single most common cause of extended timelines. The RICS valuation and mortgage application can run in parallel with the legal process, saving weeks.

Stage 4: RICS Valuation

An independent RICS Red Book valuation is mandatory for all SSAS property purchases. This is not an optional extra or a formality — it is an HMRC requirement that protects the scheme from accusations of acquiring assets at above-market prices (which would constitute an unauthorised employer-related investment or a contribution in-kind).

The RICS surveyor will produce a formal report confirming the open market value of the property. The purchase price must not exceed this value. If the valuation comes in below the agreed purchase price, the trustees have a legitimate basis to renegotiate.

For more detail on valuation requirements, see our guide on SSAS property valuation requirements. For detail on the RICS valuation specifically, see our guide on RICS valuations for SSAS property purchases.

Stage 5: Legal Due Diligence

The SSAS's solicitor conducts full legal due diligence, including:

- Title investigation: confirming the vendor has good title and there are no undisclosed charges or restrictive covenants

- Searches: local authority, drainage, environmental, and planning searches

- Lease review: if the property is tenanted, reviewing the existing lease for any onerous terms

- Planning review: confirming the property's planning use class and any conditions

- Building survey: a separate structural survey may be commissioned if the property's condition is uncertain

The solicitor will also advise on SDLT, VAT (if the property has been opted to tax), and any other tax implications of the purchase.

Stage 6: Mortgage Application and Approval

If the SSAS is borrowing to fund the purchase, the mortgage application must be submitted as early as possible. Specialist SSAS lenders will require:

- Scheme documentation (Trust Deed, HMRC registration confirmation)

- Scheme accounts and asset valuations

- The RICS valuation of the property

- Details of the proposed lease (tenant, rent, term)

- Director/trustee financial information (some lenders)

Mortgage offers typically take 4-8 weeks for SSAS applications. The lender will instruct their own solicitors to act on the security documentation in parallel with the SSAS solicitor. For more detail on typical timelines, see our guide on the SSAS property completion timeline.

Stage 7: Pensioneer Trustee Formal Approval

Before exchange of contracts, the pensioneer trustee must formally approve the transaction. They will review:

- The RICS valuation (confirming purchase at or below market value)

- The proposed lease terms (confirming commercial rent)

- The mortgage terms (confirming compliance with the 50% NAV borrowing limit)

- Any connected party aspects of the transaction

This formal approval is the pensioneer trustee exercising their governance role. It is not a rubber stamp — they may raise questions or require amendments before approving. For more on the trustee approval process, see our guide on the SSAS trustee approval process.

Stage 8: Exchange of Contracts

Once legal due diligence is complete, the RICS valuation is confirmed, and the pensioneer trustee has approved the transaction, contracts can be exchanged. Exchange is the legally binding stage — both parties are committed to complete. A deposit (typically 10%) is paid by the SSAS at exchange.

Stage 9: Completion

On the completion date, the balance of the purchase price is transferred (including any mortgage drawdown) and legal ownership passes to the SSAS trustees. The solicitor submits the SDLT return and registers the SSAS trustees as the new owners at HM Land Registry.

For more on the registration process, see our guide on SSAS title registration.

Stage 10: Grant of Lease

Following completion, the trustees grant a formal commercial lease to the tenant (whether the sponsoring employer or a third party). The lease is executed by the trustees (including the pensioneer trustee) and the tenant.

Rent collection can then begin, with income flowing directly into the SSAS bank account free of income tax.

Post-Completion Obligations

Once the purchase is complete and the lease is in place, ongoing management obligations begin. For a full overview, see our guide on post-completion SSAS property management.

"The businesses that experience the smoothest SSAS property purchases are those that treat it like a project — identifying the professional team early, understanding each stage, and managing timelines proactively. It is not a complicated process, but it does require good coordination."

— Matt Lenzie, Former Banker & Corporate Finance Partner

Ready to Start?

If you have identified a commercial property and are considering purchasing it through your SSAS, contact our team to discuss the finance options available. We can introduce you to specialist SSAS mortgage lenders and guide you through the funding structure. Visit our SSAS property finance page to learn more.

Key Takeaways

- SSAS property purchases typically take 10-16 weeks from offer acceptance to completion

- Instruct your solicitor, RICS surveyor, and mortgage broker simultaneously upon offer acceptance

- A RICS Red Book valuation is mandatory before exchange of contracts

- The pensioneer trustee must formally approve the transaction before exchange

- The SSAS mortgage application should be submitted as early as possible — underwriting takes 4-8 weeks

- A commercial lease at open market rent must be granted to the tenant after completion

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.