SSAS Loanback Compliance Checklist

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

Why a Compliance Checklist Matters

An SSAS loanback is only "permitted" under HMRC rules if it meets all six statutory conditions simultaneously. Failing even one condition means the loanback — or the non-compliant portion of it — may be treated as an unauthorised payment, triggering tax charges of 40-55% on the value involved.

This checklist is designed to be used before any loanback is arranged, and then again on an ongoing basis to monitor continued compliance. It covers the six core HMRC conditions and the key governance requirements that best practice demands.

For the underlying rules in detail, see our guide to SSAS loanback rules.

Pre-Loanback Checklist

Section 1: Scheme Eligibility

- The SSAS is currently registered with HMRC as a registered pension scheme

- The scheme trust deed permits loanbacks to the sponsoring employer

- No current HMRC investigations or enforcement actions against the scheme

- All trustees have been properly appointed and their appointments are reflected in current scheme documentation

- The scheme has a current SSAS administrator appointed

Section 2: Borrower Eligibility

- The intended borrower is the "sponsoring employer" as defined in the scheme documentation

- The employer is still an active business (not in administration, liquidation, or struck off)

- The employer is not subject to insolvency proceedings

- All directors/shareholders of the borrowing entity who are also scheme members have been identified

Section 3: The 50% Cap

- The net market value of all scheme assets has been calculated (at current market values, not historic cost)

- All existing scheme borrowings have been identified and included in the calculation

- Any existing loanbacks have been included in the loanback cap calculation

- The proposed new loanback does not, when combined with any existing loanbacks, exceed 50% of net scheme assets

- The calculation is documented and signed off by the SSAS administrator

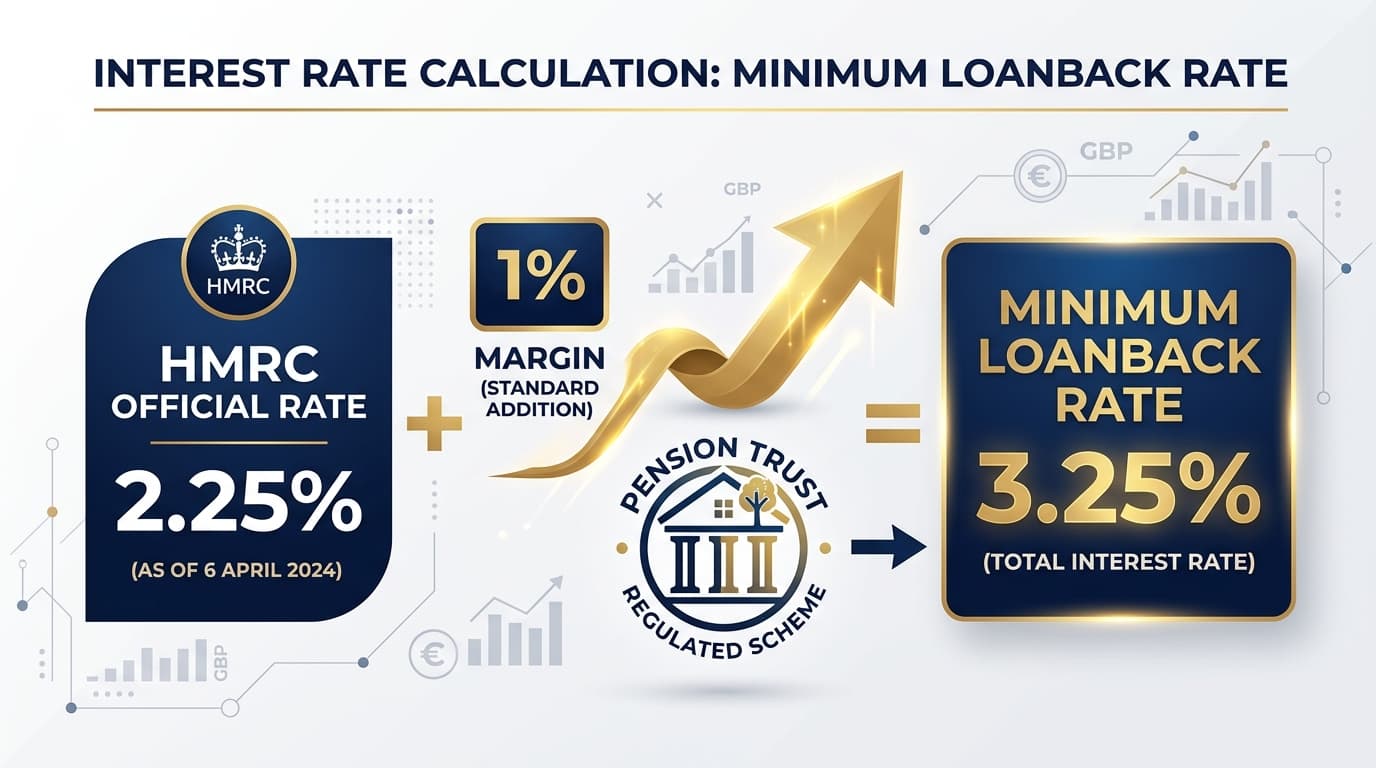

Section 4: Interest Rate

- The interest rate to be charged has been identified

- The rate is no less than the HMRC official rate plus 1% (currently minimum 3.25% for 2025/26)

- The rate is documented in the loan agreement as either a fixed rate or a variable rate linked to the official rate plus 1%

- If a fixed rate is used, the rate equals or exceeds the minimum at the date of the loan

Section 5: Repayment Terms

- The loan term does not exceed five years from the date of first drawdown

- The repayment structure provides for equal capital instalments (not interest-only with balloon repayment)

- A formal repayment schedule has been prepared showing each instalment date, amount, and resulting balance

- The final repayment date under the schedule falls within the five-year maximum term

- The employer has assessed its cash flow and confirmed it can meet each instalment on time

Section 6: Security

- A specific asset (or assets) has been identified to serve as security for the loanback

- The identified security is owned by the sponsoring employer or a connected person

- A professional valuation has been obtained confirming the security's current market value equals or exceeds the loan amount

- A title search or Companies House search has confirmed no existing first charge on the proposed security

- The intended charge is a first legal charge (not a second charge or floating charge only)

- Legal documentation for the charge has been prepared and will be executed before drawdown

- The charge will be registered (Land Registry for property; Companies House for debentures) promptly after execution

Section 7: Business Purpose

- The intended use of the loanback funds is a legitimate business purpose of the sponsoring employer

- The purpose has been documented in the loan agreement or board minutes of the employer

- There is no personal benefit to any scheme member from the use of the funds

- Trustees have independently satisfied themselves that the purpose is commercial

Section 8: Loan Documentation

- A formal written loan agreement has been prepared by a qualified solicitor

- The loan agreement specifies the loan amount, interest rate, term, instalment dates, and security

- A repayment schedule is appended to the loan agreement

- The agreement is signed by all trustees on behalf of the scheme

- The agreement is signed by an authorised signatory of the sponsoring employer

- The agreement is dated before (or on the same day as) the drawdown date

Section 9: Trustee Governance

- A trustee meeting has been held to formally approve the loanback

- Minutes of the trustee meeting document the decision and the trustees' reasoning

- All trustees have voted to approve (or the trust deed's required majority has been obtained)

- Any trustee with a conflict of interest (e.g., a trustee who is also a director of the borrowing company) has been appropriately managed per the trust deed

- The SSAS administrator has been notified and has confirmed compliance with the 50% cap

Ongoing Compliance Checklist

Once the loanback is in place, the following ongoing monitoring is required:

- All instalments are received on the due date and in the correct amount

- Any missed or late payment is reported to trustees immediately

- Trustees take prompt action on any default — in writing to the employer

- The loanback balance is maintained as an asset in the annual SSAS accounts

- Interest income is recorded in the scheme's accounting records

- The security charge remains in place and has not been discharged prematurely

- The security asset has not declined in value to below the outstanding loan amount (regular checks recommended)

- No changes to loan terms have been made without proper trustee approval and documentation

Exit Checklist: On Full Repayment

- Final instalment has been received and reconciled to the repayment schedule

- A formal receipt confirming full repayment is issued to the employer

- The security charge is formally discharged (Land Registry / Companies House)

- The SSAS accounts are updated to remove the loanback receivable

- Trustee minutes record the successful completion and repayment of the loanback

Red Flags That Require Immediate Attention

If any of the following occur during the loanback term, take immediate specialist advice:

- The employer misses an instalment or requests a payment holiday

- The employer enters financial distress or insolvency proceedings

- The security asset's value falls significantly below the outstanding loan balance

- A trustee wants to unilaterally modify the loanback terms

- A dispute arises between trustees about the management of the loanback

- HMRC enquires about the loanback or requests information about it

Matt Lenzie notes: "In my experience, loanback problems almost always stem from poor initial documentation or inadequate monitoring rather than the original structure being wrong. A well-documented, properly monitored loanback is straightforward to administer and defend if HMRC ever reviews it."

Key Takeaways

- All six HMRC conditions must be met simultaneously — there's no partial compliance

- Documentation is critical — verbal arrangements and informal documentation are not sufficient

- Ongoing monitoring by the SSAS administrator is as important as the initial set-up

- Take specialist advice immediately if any compliance risk materialises during the loanback term

- Use this checklist before every new loanback, not just the first

Arrange a Fully Compliant SSAS Loanback

Our team helps SSAS trustees structure, document, and monitor loanbacks to the highest compliance standards. We work with you through every stage from initial assessment to final repayment.

Contact us today to discuss your loanback requirements, or read our in-depth SSAS loanback rules guide for the full regulatory context.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.