SSAS Loanback Worked Example: A Complete Case Study

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

A Complete SSAS Loanback Case Study

The best way to understand how an SSAS loanback works is to walk through a complete, realistic example with real numbers. This case study follows a four-member SSAS from initial assessment through to final repayment, covering every key calculation and compliance requirement.

For the underlying rules that govern every element of this example, see our comprehensive guide to SSAS loanback rules.

The Business and Scheme Background

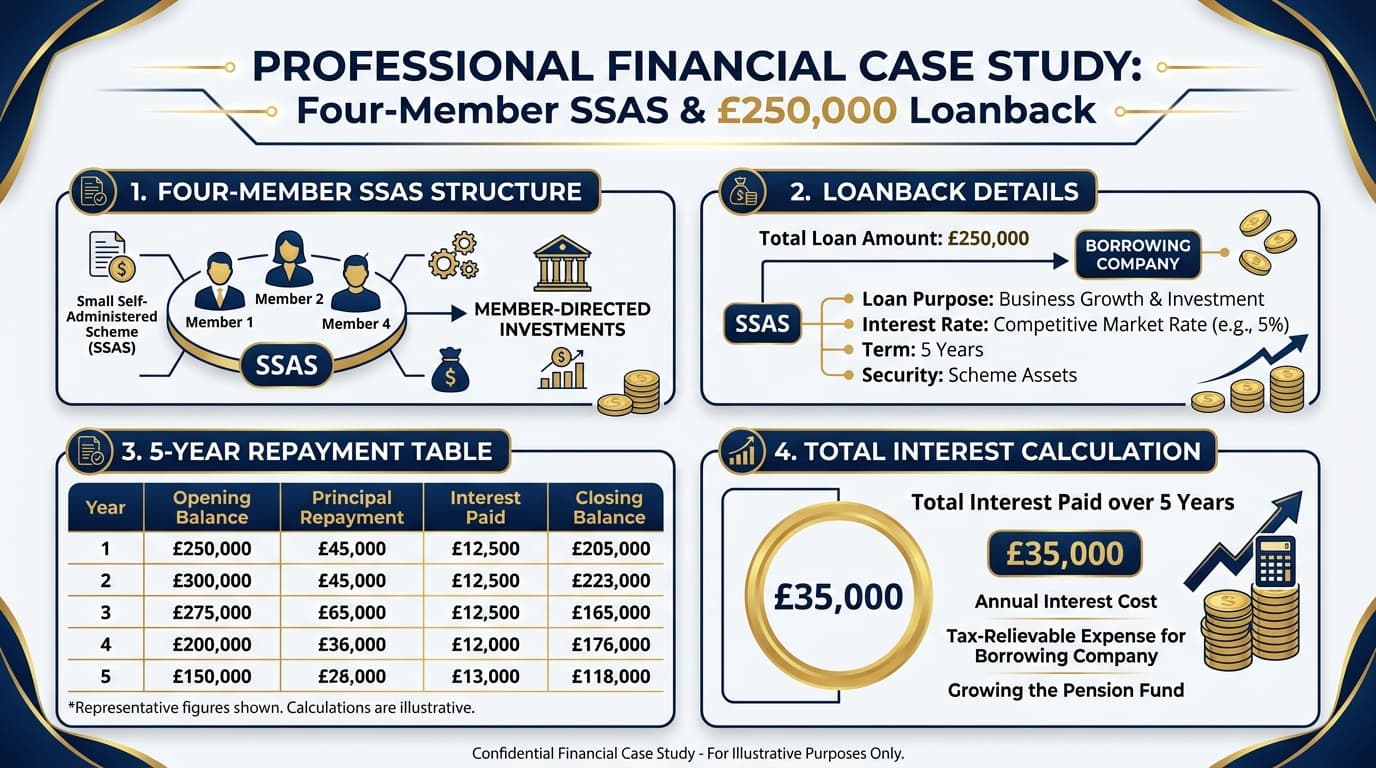

Four directors — Alex, Bea, Chris, and Diana — are co-owners of a successful engineering company, Precision Works Ltd. They established an SSAS pension scheme five years ago and have been contributing regularly since then.

Precision Works SSAS — Current Position:

- Alex's share: £210,000

- Bea's share: £195,000

- Chris's share: £180,000

- Diana's share: £165,000

- Total scheme assets: £750,000 (held entirely in cash and quoted investments)

- Existing scheme borrowing: NIL

- Existing loanbacks: NIL

The Business Need: Precision Works Ltd has an opportunity to acquire a smaller competitor for £250,000. The acquisition would significantly increase revenue and profit. However, the company's working capital is tied up in stock and debtors, and the bank has declined to provide acquisition finance at attractive terms. The directors have identified the SSAS loanback as a potential solution.

Step 1: Can the SSAS Lend This Amount?

The 50% Cap Calculation

Net scheme assets = £750,000 (no existing liabilities)

Maximum loanback = 50% × £750,000 = £375,000

The proposed loanback of £250,000 is comfortably within the 50% cap. The scheme retains £125,000 of unused loanback capacity.

The trustees also want to check whether the loanback leaves the scheme with adequate liquidity. After the loanback drawdown, the scheme would hold:

- Loanback receivable: £250,000

- Cash and investments: £500,000

- Total: £750,000 (net assets unchanged — the loanback is an asset swap, cash to receivable)

The scheme retains £500,000 in liquid assets — sufficient for any foreseeable near-term benefit payment obligations. The trustees are satisfied.

Step 2: Establishing the Terms

Interest Rate

The loan is to be arranged in October 2025, in the 2025/26 tax year. The HMRC official rate is 2.25%. The minimum loanback interest rate is therefore 3.25% per annum.

The trustees agree to set the interest rate at 3.5% — slightly above the minimum — to reflect the fact that this is an acquisition loan and carries slightly more risk than simple working capital. The rate is fixed for the five-year term.

Term and Repayment

The loan is for five years (the maximum). Monthly equal capital instalments of £250,000 ÷ 60 = £4,166.67 per month (approximately £4,167), plus interest on the reducing balance.

Step 3: The Repayment Schedule

Monthly interest calculation: Outstanding balance × (3.5% ÷ 12)

Year 1 Summary

- Opening balance: £250,000

- Monthly capital repayment: £4,167

- Total capital repaid in Year 1: £50,000 (12 months × £4,167)

- Average balance during Year 1: £225,000

- Approximate total interest in Year 1: £225,000 × 3.5% = £7,875

- Closing balance after Year 1: £200,000

- Total paid in Year 1 (capital + interest): £57,875

Year 2 Summary

- Opening balance: £200,000

- Capital repaid: £50,000

- Average balance: £175,000

- Approximate interest: £6,125

- Closing balance: £150,000

- Total paid: £56,125

Year 3 Summary

- Opening balance: £150,000

- Capital repaid: £50,000

- Average balance: £125,000

- Approximate interest: £4,375

- Closing balance: £100,000

- Total paid: £54,375

Year 4 Summary

- Opening balance: £100,000

- Capital repaid: £50,000

- Average balance: £75,000

- Approximate interest: £2,625

- Closing balance: £50,000

- Total paid: £52,625

Year 5 Summary

- Opening balance: £50,000

- Capital repaid: £50,000

- Average balance: £25,000

- Approximate interest: £875

- Closing balance: £0 (fully repaid)

- Total paid: £50,875

Five-Year Totals

- Total capital repaid: £250,000

- Total interest paid to scheme: approximately £21,875

- Total cost to the business over five years: £271,875

- Total returned to the pension scheme: £271,875

Step 4: Security

The trustees require first charge security equal to at least £250,000. Precision Works Ltd owns a freehold industrial unit valued at £380,000 (no existing mortgage). The trustees agree to take a first legal charge over this property as security for the loanback.

The charge is executed as a legal deed, signed by all trustees of the scheme and the directors of Precision Works Ltd, and registered at HM Land Registry before the loan is drawn down.

Step 5: Business Impact Analysis

From Precision Works Ltd's perspective:

- Corporation tax relief on interest: £21,875 interest × 25% corporation tax rate = £5,469 tax saving over five years

- Net cost of the loanback after tax relief: approximately £266,406

- Equivalent bank loan cost (estimated 8.5% per annum over 5 years): approximately £296,000 total cost

- Estimated saving vs bank finance: approximately £30,000 over five years

Additionally, the interest paid is received tax-free by the pension scheme — a further benefit that isn't captured in the direct cost comparison.

Step 6: Scheme Impact Analysis

From the Precision Works SSAS perspective:

- The £250,000 loanback receivable earns 3.5% per annum — outperforming many cash deposit rates

- Total interest income over five years: £21,875 — received tax-free within the scheme

- Capital is fully returned within five years, available for reinvestment

- The scheme's net assets remain at £750,000 throughout (loanback receivable + cash/investments)

- After full repayment, the scheme holds £750,000 + £21,875 interest = £771,875 — a 2.9% gain on the loanback investment alone

Matt Lenzie notes: "This case study illustrates why the loanback is sometimes described as a 'win-win' for business owner-members. The business gets cheaper finance than the bank would provide, and that saving flows directly back into their pension scheme. It's essentially paying themselves interest."

Step 7: Completing the Transaction

The trustees hold a formal meeting, resolve to approve the loanback, and record their decision in minutes. The key documents produced are:

- Trustee resolution approving the loanback

- Formal loan agreement between the SSAS trust and Precision Works Ltd

- Repayment schedule appendix

- First legal charge over the industrial property

- Land Registry registration of the charge

- Employer board minutes approving the borrowing

The £250,000 is transferred from the scheme bank account to Precision Works Ltd's business account on the completion date.

Monitoring Throughout the Term

The SSAS administrator monitors monthly repayments against the schedule. All 60 instalments are received on time. At the end of year 5, the final instalment is paid, the charge is discharged from Land Registry, and the trustees record the successful completion in their meeting minutes.

Key Takeaways from This Case Study

- A £250,000 loanback is well within the 50% cap for a £750,000 SSAS

- Total interest cost to the business over five years is approximately £21,875 — all received tax-free by the scheme

- Net cost after corporation tax relief compares very favourably to bank borrowing

- First charge security over an unencumbered property provides robust protection for the scheme

- Good documentation and monitoring by the SSAS administrator ensures seamless compliance throughout

Is a Loanback Right for Your Business?

Our team can run this analysis for your specific scheme and business requirements — quickly and confidentially.

Contact us today to discuss your SSAS loanback options, or use our SSAS mortgage calculator to compare loanback with mortgage financing alternatives.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.