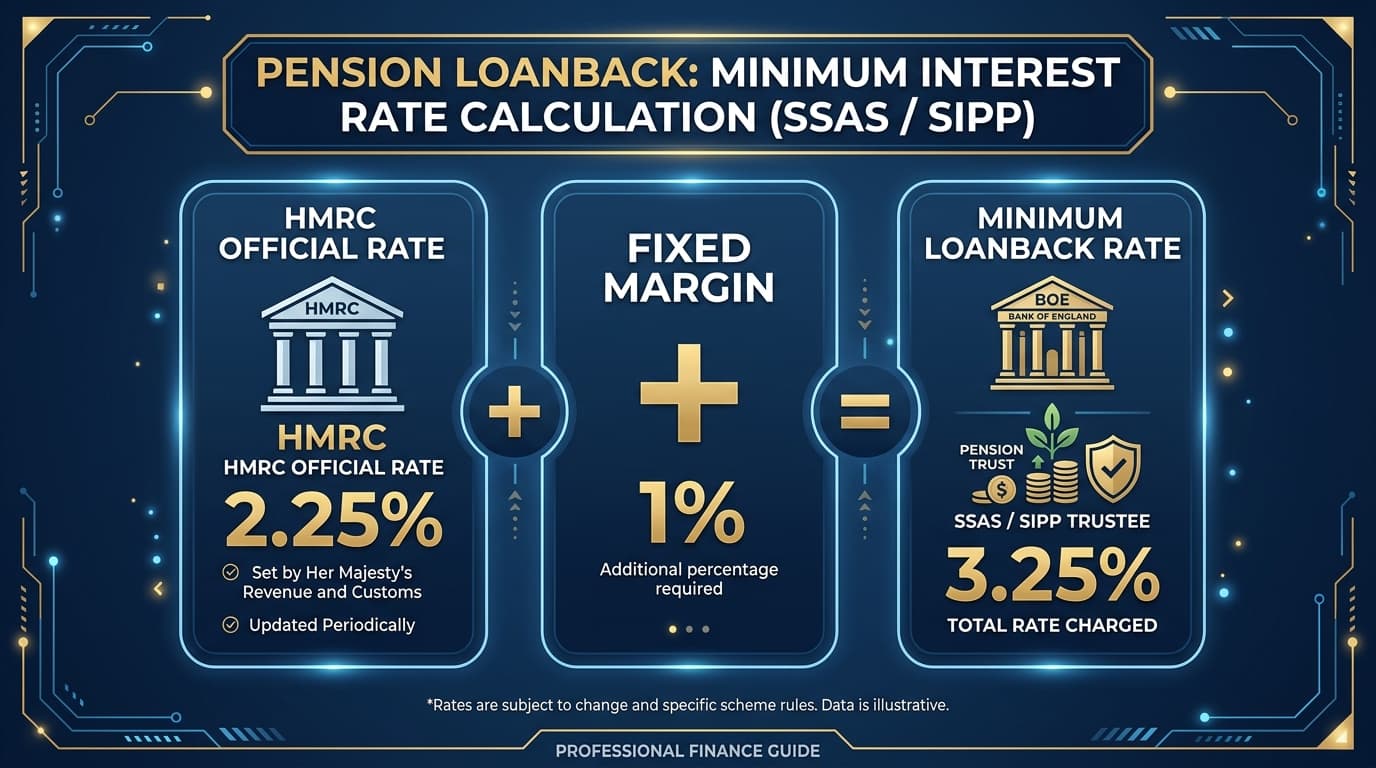

Base Rate Plus 1%: Understanding the SSAS Loanback Minimum Interest Rate

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

The "Base Rate Plus 1%" Rule in Context

When people refer to the "base rate plus 1% rule" for SSAS loanbacks, they're describing HMRC's requirement that the interest rate charged on any loanback must be at least 1% above the "official rate." In everyday language, this has become shorthand as "base rate plus 1%" — though technically it's the HMRC official rate, not the Bank of England base rate, that applies.

This distinction is important because the official rate and the Bank of England base rate are not always the same.

For the full context of loanback interest rate rules, see our dedicated guide to SSAS loanback interest rate rules.

What Is the HMRC Official Rate?

The official rate is set by HMRC under the Income Tax (Earnings and Pensions) Act 2003. It is used across a range of HMRC calculations — most notably the "beneficial loan" rules that apply to loans from employers to employees — but it also sets the floor for SSAS loanback interest rates.

The official rate is reviewed by HMRC and updated periodically (not automatically linked to Bank of England base rate changes). For the 2025/26 tax year, the official rate is 2.25%.

Therefore: Minimum SSAS loanback interest rate for 2025/26 = 2.25% + 1% = 3.25% per annum.

How the Official Rate Is Set and Updated

HMRC sets the official rate via Treasury Order. Historically it was changed infrequently, but in recent years it has been updated more regularly to better track market rates. Key points:

- Changes to the official rate are announced by HMRC and typically effective from the start of a tax year

- HMRC publishes the current rate on its website (search "HMRC official rate of interest")

- The rate cannot fall below 1% under current legislation

Matt Lenzie notes: "A common misconception is that when the Bank of England cuts rates, the SSAS loanback minimum rate automatically falls. That's not how it works. The HMRC official rate moves independently — sometimes in the same direction as Bank of England base rate, sometimes with a lag, and always via a formal Treasury Order rather than automatically."

Why HMRC Imposes This Minimum

The minimum interest rate requirement serves two important purposes:

Protecting Pension Scheme Members

The pension scheme is lending its assets to the employer. If the interest rate were below market (or zero), the scheme would effectively be subsidising the employer — at the expense of all pension members' retirement savings. The minimum rate ensures the scheme receives a commercial return on the loanback as an investment.

Preventing Disguised Benefit

If the employer borrowed below-commercial-rate loans from the pension scheme, the below-market interest saving would represent a benefit — either to the employer's shareholders (who happen to be pension members) or directly to the pension members themselves. This could be construed as an unauthorised payment from the scheme.

Can You Charge More Than the Minimum?

Yes. The minimum rate is a floor, not a ceiling. Trustees can (and sometimes should) charge a higher rate if the commercial circumstances justify it.

Reasons to charge above the minimum:

- The employer represents a higher credit risk and a commercial lender would require a higher rate

- The security provided is weaker than ideal and the higher rate compensates the scheme for the additional risk

- The scheme has an investment mandate that requires above-minimum returns on fixed income investments

In practice, most SSAS loanbacks are arranged at the minimum rate because the employer-trustee relationship makes the minimum commercially reasonable — the main objective is to recycle interest back into the pension at the minimum compliant rate rather than to maximise interest income.

Fixed Rate at Inception vs. Variable Rate

SSAS loanbacks can be structured with either a fixed or variable interest rate:

Fixed Rate

Set at the official rate plus 1% at the time of the loan. It doesn't automatically adjust if the official rate subsequently changes. For example, a loanback arranged in the 2025/26 tax year at 3.25% fixed remains at 3.25% even if the official rate changes in a subsequent year.

HMRC's position is that the rate is tested at the time of the loan — provided it met the minimum at inception, a fixed rate remains compliant even if the official rate subsequently rises above the fixed rate. However, trustees and administrators should monitor this and take advice if the fixed rate falls significantly below the prevailing minimum.

Variable Rate Linked to Official Rate

Can be structured to always be 1% above the official rate, updating automatically when HMRC changes it. This ensures the loanback always meets the minimum, but introduces payment uncertainty for the employer.

Current Rate Context

For context on where the current minimum rate sits relative to wider market rates:

- Bank of England base rate: Approximately 4.25-4.5% (early 2025)

- HMRC official rate: 2.25% (2025/26)

- SSAS loanback minimum: 3.25%

- Typical SME bank loan rate: 6.5-10%+

- SSAS mortgage rate: Approximately 5.5-7%

The SSAS loanback minimum remains attractive relative to bank borrowing for most SMEs, particularly when the interest flows back into the pension scheme rather than to a bank.

For a comparison of loanback versus other SSAS financing options, see our guide to SSAS loanback vs mortgage.

The Interest Rate in the Loan Agreement

The loan agreement must clearly state the interest rate and how it is calculated. We recommend the agreement specifies:

- Whether the rate is fixed or variable

- If fixed: the exact rate (e.g., "3.25% per annum fixed")

- If variable: the reference rate (HMRC official rate) and the margin above it (1%)

- How and when rate changes are communicated (for variable rate arrangements)

- Whether interest accrues daily, monthly, or annually

Ambiguity in the interest rate clause is a compliance risk. Courts and HMRC take a strict approach to the enforceability of interest provisions in pension scheme loans.

Key Takeaways

- The minimum SSAS loanback interest rate is the HMRC official rate (currently 2.25%) plus 1% = 3.25% for 2025/26

- The official rate is set by HMRC, not automatically linked to Bank of England base rate

- Higher rates are permitted and sometimes appropriate depending on credit risk and security quality

- Fixed rates are tested at inception — a compliant fixed rate remains compliant through the loan term

- The loan agreement must unambiguously specify the interest rate and calculation method

Ensure Your Loanback Rate Is Compliant

Our team can advise on setting the correct interest rate for your SSAS loanback and ensure the loan documentation meets HMRC requirements.

Contact us today to discuss your loanback, or review our complete SSAS loanback compliance checklist.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.