SSAS Bridging Finance: When It Works and How to Use It

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

SSAS Bridging Finance: A Practical Guide

Speed is often decisive in commercial property transactions. When a property comes to market at an attractive price, competition can be intense, and the ability to complete quickly is frequently the difference between securing the deal and losing it. SSAS bridging finance provides exactly this capability — short-term funding that allows your pension scheme to complete a property purchase rapidly, with a longer-term mortgage arranged separately.

This guide explains when SSAS bridging finance is appropriate, how it is structured, what it costs, and how to plan the exit from the bridge to long-term finance.

What Is SSAS Bridging Finance?

Bridging finance is a short-term loan — typically running from one month to twenty-four months — designed to "bridge" the gap between the need for funds and a longer-term financing solution. In the context of SSAS property investment, bridging finance is used when:

- A time-sensitive property opportunity arises that cannot wait for the typical eight to twelve-week timeline of a commercial mortgage

- The property has a short-term issue (title defect, planning question, tenancy void) that prevents mainstream mortgage lenders from lending immediately

- The SSAS is purchasing at auction, where completion typically must occur within twenty-eight days

- The scheme needs to complete before an existing property is sold or before alternative funds are realised

How SSAS Bridging Finance Differs from Standard Bridging

SSAS bridging finance operates within the same regulatory framework as any other SSAS borrowing — the loan must not exceed 50% of the net scheme assets, and the property acquired must be eligible for pension scheme ownership (commercial, not residential). The lender must also be willing to lend to a pension scheme, which narrows the field compared to the broader bridging market.

The trustee structure of a SSAS means that all trustees must execute the loan documentation, and the lender will require trustee resolutions authorising the borrowing. This adds a layer of process compared to individual or company bridging, but should not materially delay completion with a prepared scheme.

Typical Terms for SSAS Bridging Finance

SSAS bridging finance terms in 2025 typically look as follows:

- Loan term: 3 to 24 months

- Maximum LTV: 50-65% of the property value (subject to the 50% of net scheme assets rule)

- Interest rate: Typically 0.75% to 1.50% per month (9% to 18% per annum)

- Interest structure: Rolled up (added to the loan and repaid at exit) or monthly serviced

- Arrangement fee: 1-2% of the loan amount

- Exit fee: Some lenders charge an exit fee of 0.5-1% on repayment

Given the higher cost of bridging finance relative to long-term mortgages, it is almost always used as a short-term measure with a clear exit strategy to a standard commercial mortgage.

"Bridging finance for SSAS is a genuine competitive advantage in the auction room and for off-market deals where speed matters. The key is having the exit strategy — the long-term mortgage — planned in advance so you are not rolling the bridge longer than necessary." — Matt Lenzie, Former Banker & Corporate Finance Partner

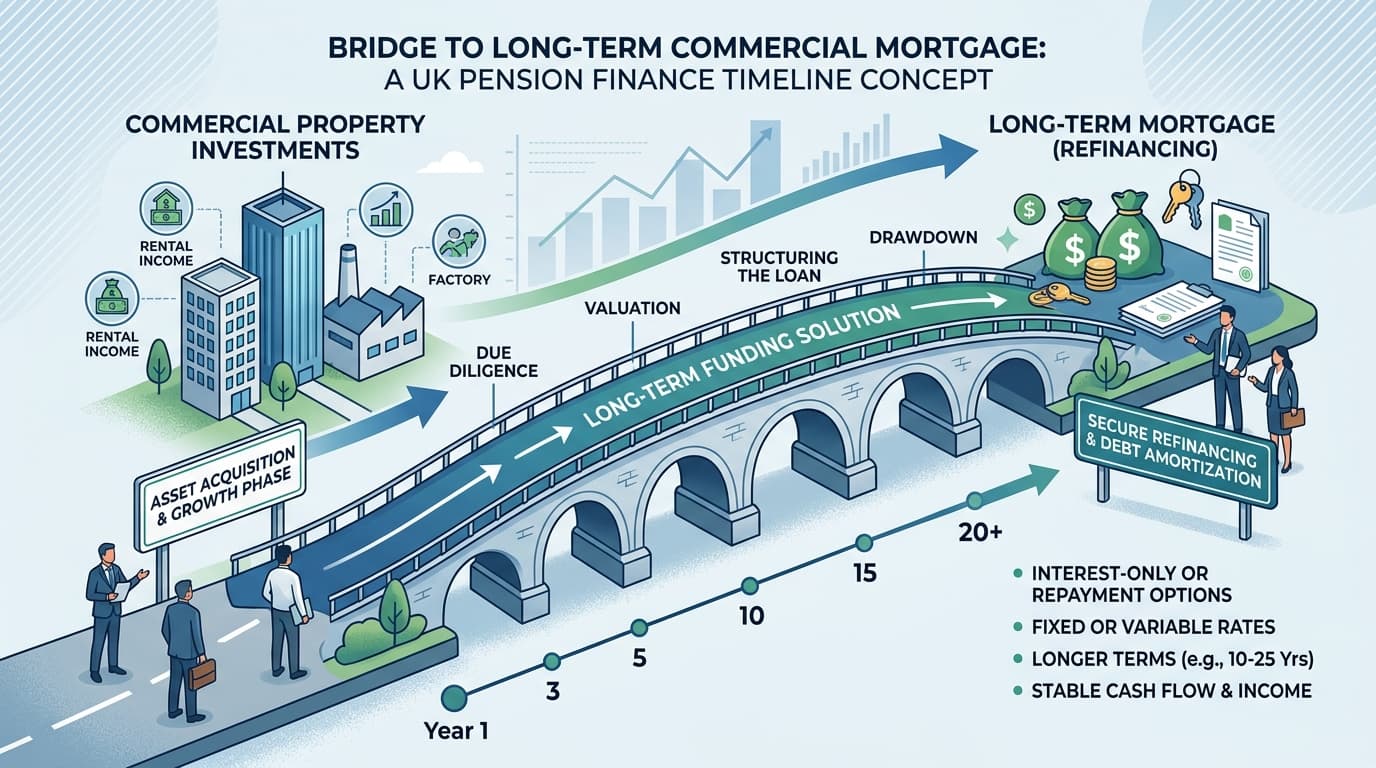

The Exit Strategy: Moving to Long-Term Finance

The exit from a SSAS bridge loan is almost always a commercial mortgage — either from the same lender (many bridging lenders have a commercial mortgage arm) or from a different lender in the market. The exit strategy should be considered and tested before the bridging finance is drawn down.

Key questions for the exit strategy include:

- Will the property meet standard commercial mortgage criteria once the bridging issue is resolved?

- What LTV and rate will the long-term mortgage be available at?

- Is there sufficient rental income from the tenant to service the long-term mortgage?

- Is there a realistic timeline for the exit before the bridge term expires?

It is important to have the long-term mortgage agreed in principle before drawing down the bridge — this prevents the risk of being "stranded" on a bridge if the long-term market moves against you.

Bridging at Auction

Commercial property auctions represent a significant source of investment opportunities for SSAS schemes — often at prices below what the open market would achieve for equivalent properties. The requirement for completion within twenty-eight days of the auction makes bridging finance the standard funding route.

To use bridging finance at auction, the SSAS should have a decision in principle from a bridging lender before bidding. This requires preparing and submitting the scheme information pack in advance and having the trustee resolutions ready to execute promptly after the hammer falls.

Costs and Value for Money

Bridging finance is expensive relative to long-term commercial mortgages. A bridge at 1.0% per month costs 12% per annum — compared to perhaps 6-8% for a term commercial mortgage. For a short bridge of two to three months, this additional cost is generally justified by the opportunity created. For a bridge that runs to twelve months or beyond, the costs become very significant and may erode the investment return materially.

Always model the total cost of the bridge (including rolled-up interest, arrangement fees, and exit fees) against the premium you would expect to pay for equivalent open-market property to ensure the deal remains compelling.

Finding the Right Bridging Lender

Not all bridging lenders will lend to SSAS pension schemes. The pool of willing SSAS bridging lenders is smaller than the broader market, and specialist knowledge is required to identify the right lender for your specific transaction. Our lender panel includes specialist SSAS bridging providers who understand pension scheme requirements.

Key Takeaways

- SSAS bridging finance provides short-term funding for time-sensitive property purchases

- Typical terms are 3-24 months at 0.75-1.50% per month interest

- The exit strategy — transition to a long-term commercial mortgage — must be planned before drawdown

- Bridging at auction is a powerful SSAS competitive advantage when properly prepared

- Not all bridging lenders will lend to SSAS schemes — specialist access is needed

Access SSAS Bridging Finance Fast

Our team can access specialist SSAS bridging lenders and manage the entire process from initial enquiry to drawdown.

Contact us today to discuss your SSAS bridging requirement, or explore the range of SSAS property finance options available.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.