The SSAS Mortgage Application Process: A Step-by-Step Guide

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

Why SSAS Mortgage Applications Are Different

An SSAS mortgage isn't like a standard buy-to-let or commercial mortgage. The lender isn't just assessing a borrower and a property — they're assessing a pension scheme governed by HMRC rules, with multiple trustees, a complex asset structure, and potential regulatory consequences if anything goes wrong.

In our experience, the biggest delays and failures in SSAS mortgage applications come from trustees who underestimate this complexity and approach the process without adequate preparation. This guide explains every step so you know exactly what to expect.

Stage 1: Pre-Application Assessment

Before approaching any lender, you should complete an internal assessment covering:

Scheme Compliance Check

- Confirm the scheme is currently registered with HMRC

- Verify the scheme deed permits property investment and borrowing

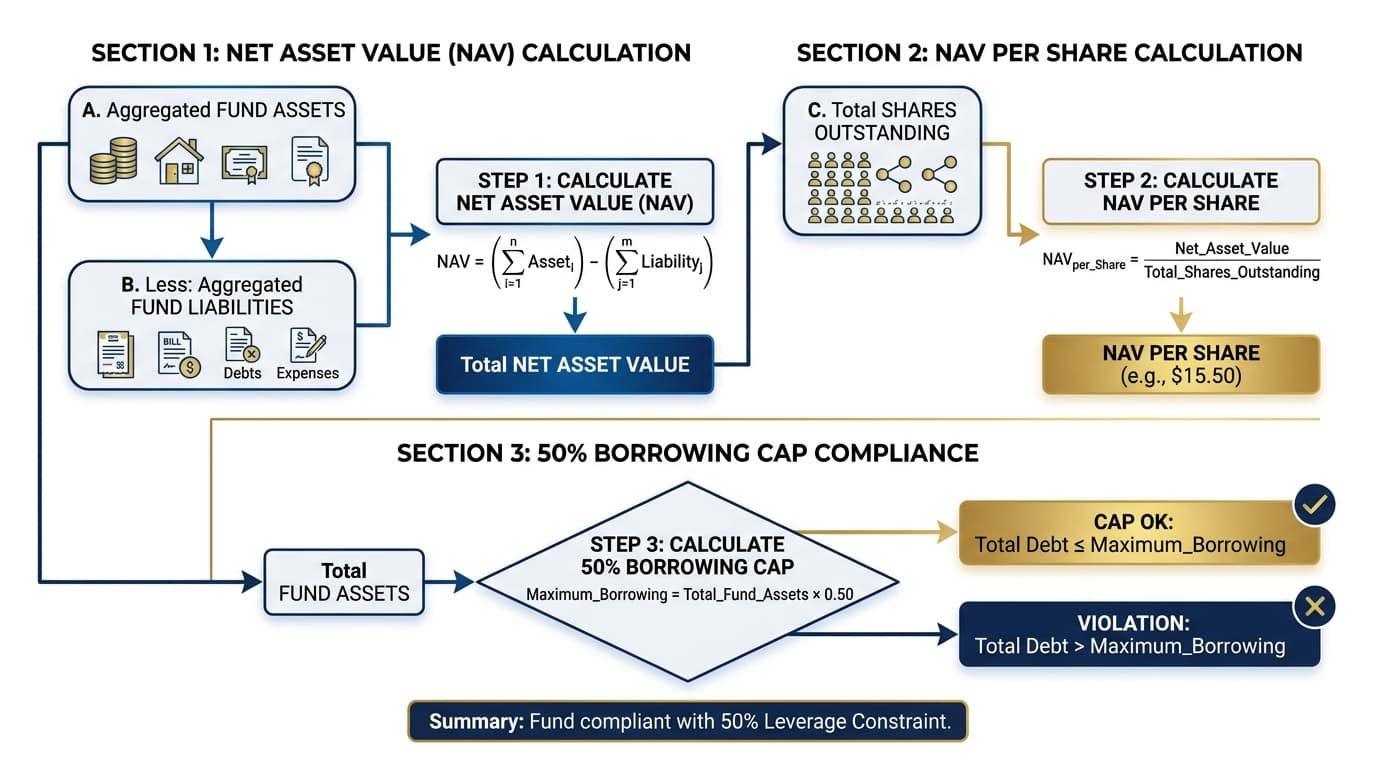

- Check the HMRC 50% borrowing cap — calculate your available headroom

- Confirm no current unauthorised payment issues or HMRC investigations

Property Suitability Assessment

- Confirm the property is commercial (residential property cannot be held in SSAS)

- Check that the intended use falls within HMRC's permitted property types

- Obtain an initial sense of market value to understand what borrowing might look like

For a full overview of the process, see our guide to SSAS property finance.

Stage 2: Identifying the Right Lender

Not all commercial mortgage lenders will lend to SSAS schemes. A relatively small number of specialist lenders and challenger banks have the expertise to navigate the regulatory requirements. Selecting the wrong lender can waste weeks.

Matt Lenzie notes: "High street banks rarely have SSAS-knowledgeable underwriters. We've seen applications submitted to mainstream lenders that sat for months before being declined on a technicality that a specialist lender would have cleared in days."

Key considerations when identifying a lender:

- Does the lender have a specific SSAS or SIPP lending product?

- What is their maximum LTV for pension scheme lending?

- Do they require a personal guarantee from trustees or members?

- What are their typical interest rates and arrangement fees for SSAS?

Our lender panel includes the leading SSAS mortgage providers in the UK. We can match you with the most appropriate lender for your scheme and property type.

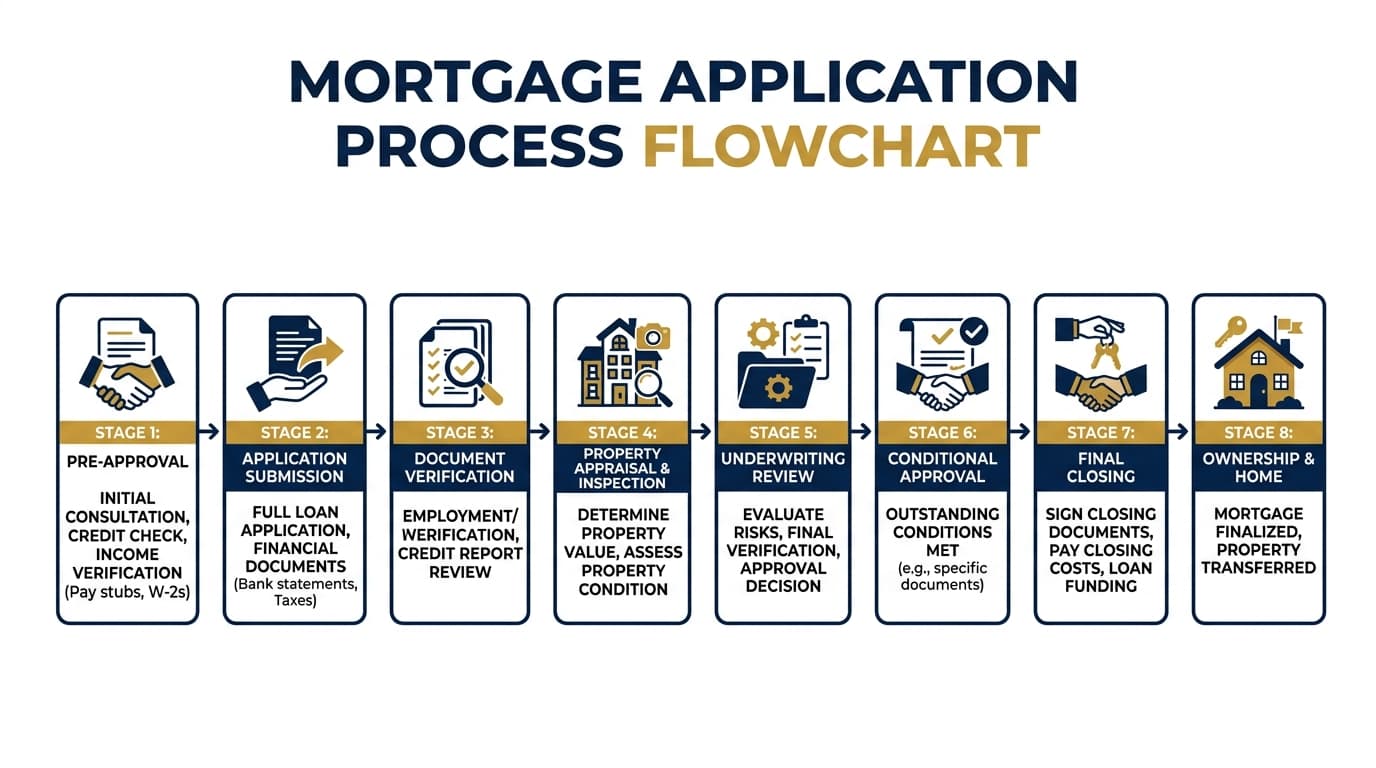

Stage 3: Decision in Principle

Most lenders will issue a Decision in Principle (DIP) or Indicative Terms before proceeding to full application. For a DIP, you'll typically need to provide:

- Scheme name and HMRC registration number

- Names of all trustees and members

- Approximate scheme asset value and existing borrowing

- Property address and estimated value

- Proposed loan amount and term

- Details of existing or proposed tenancy arrangements

A DIP is usually issued within 3-5 working days and is subject to full underwriting — it's not a guarantee of lending. However, it confirms the lender is willing to consider the application in principle and gives you a basis for negotiating with the property vendor.

Stage 4: Full Application and Documentation

Once you have a DIP and are ready to proceed, the lender will issue a full application form along with a document checklist. Typical requirements include:

Scheme Documents

- Trust deed and rules

- HMRC scheme registration confirmation

- Latest actuarial valuation or scheme accounts (usually within 12-18 months)

- Schedule of current scheme assets and liabilities

- Trustee meeting minutes authorising the proposed borrowing

Property Documents

- Heads of terms from the vendor or agent

- Existing title documents (if available)

- Copies of current leases or proposed lease terms

- Any planning permissions or building regulations certificates

Financial Information

- 3 years of accounts for the sponsoring employer (if it's the tenant)

- Evidence of rental income (if letting to third parties)

- Bank statements for the scheme's bank accounts

Member/Trustee Information

- Proof of identity and address for all trustees (passport, utility bills)

- AML/KYC documentation as required by the lender

Stage 5: Valuation

The lender will instruct a Royal Institution of Chartered Surveyors (RICS) qualified surveyor to carry out a formal valuation of the property. This is typically at the borrower's expense (£1,500–£3,500 depending on property size and complexity).

The valuation report will confirm:

- Market value on the open market

- Estimated rental value (ERV) if the property is vacant

- Any material defects or concerns

- Lender's assessed value (which may differ from asking price)

If the valuation comes in below the agreed purchase price, the lender's maximum loan will be calculated against the lower valuation figure — so the scheme will need additional funds to bridge any gap.

Stage 6: Formal Mortgage Offer

Once the valuation, legal due diligence, and underwriting are complete, the lender issues a formal mortgage offer. This will specify:

- Loan amount, interest rate, and term

- Arrangement fee, valuation fee, and legal fees

- Any special conditions to be satisfied before drawdown

- Insurance requirements

Review the offer carefully with your SSAS administrator and legal advisers. Conditions may include things like a formal lease being executed, buildings insurance being confirmed, or scheme accounts being updated.

Stage 7: Legal Process and Completion

Both the lender and the SSAS will have their own solicitors. The legal process typically involves:

- Review of title and property searches

- Negotiation and execution of the mortgage deed

- Review and execution of lease documentation

- Transfer of funds and completion

SSAS mortgage legal work typically takes 6-12 weeks from formal offer, though complex transactions can take longer. Using solicitors experienced in SSAS and pension scheme property conveyancing is strongly recommended.

Typical Timeline Overview

- Pre-assessment and lender identification: 1-2 weeks

- Decision in Principle: 3-5 working days

- Full application submission: 1-2 weeks

- Underwriting and valuation: 3-6 weeks

- Formal offer: 1-2 weeks after valuation

- Legal process and completion: 6-12 weeks

Total typical timeline: 3-5 months from initial enquiry to completion.

Key Takeaways

- SSAS mortgage applications are more complex than standard commercial mortgages — specialist lenders are essential

- Preparation is everything: have your scheme documents and financial information ready before approaching lenders

- The typical timeline is 3-5 months, so factor this into property purchase negotiations

- Valuation fees, arrangement fees, and legal costs should be budgeted for upfront

- Using experienced SSAS advisers, administrators, and solicitors significantly reduces risk of delays

Start Your SSAS Mortgage Application

Whether you're at the early planning stage or ready to apply, our team can guide you through the entire process and introduce you to the right lender for your scheme.

Contact us today for a confidential consultation. You can also use our SSAS mortgage calculator to model indicative borrowing costs before you begin.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.