SSAS Fixed vs Variable Rates: Which Is Right for Your Scheme?

Written by Matt Lenzie

Former Banker & Corporate Finance Partner

SSAS Fixed vs Variable Rates: Making the Right Choice

When financing a property purchase through your SSAS, one of the earliest decisions you will face is whether to take a fixed or variable interest rate. This choice affects your monthly repayments, the flexibility of the facility, and ultimately the total cost of borrowing over the mortgage term. There is no universally correct answer — the right choice depends on your scheme's circumstances, risk tolerance, and financial planning objectives.

This guide explains the key differences between fixed and variable rate SSAS mortgages, the circumstances that favour each, and how to think through the decision for your specific situation.

Fixed Rate SSAS Mortgages

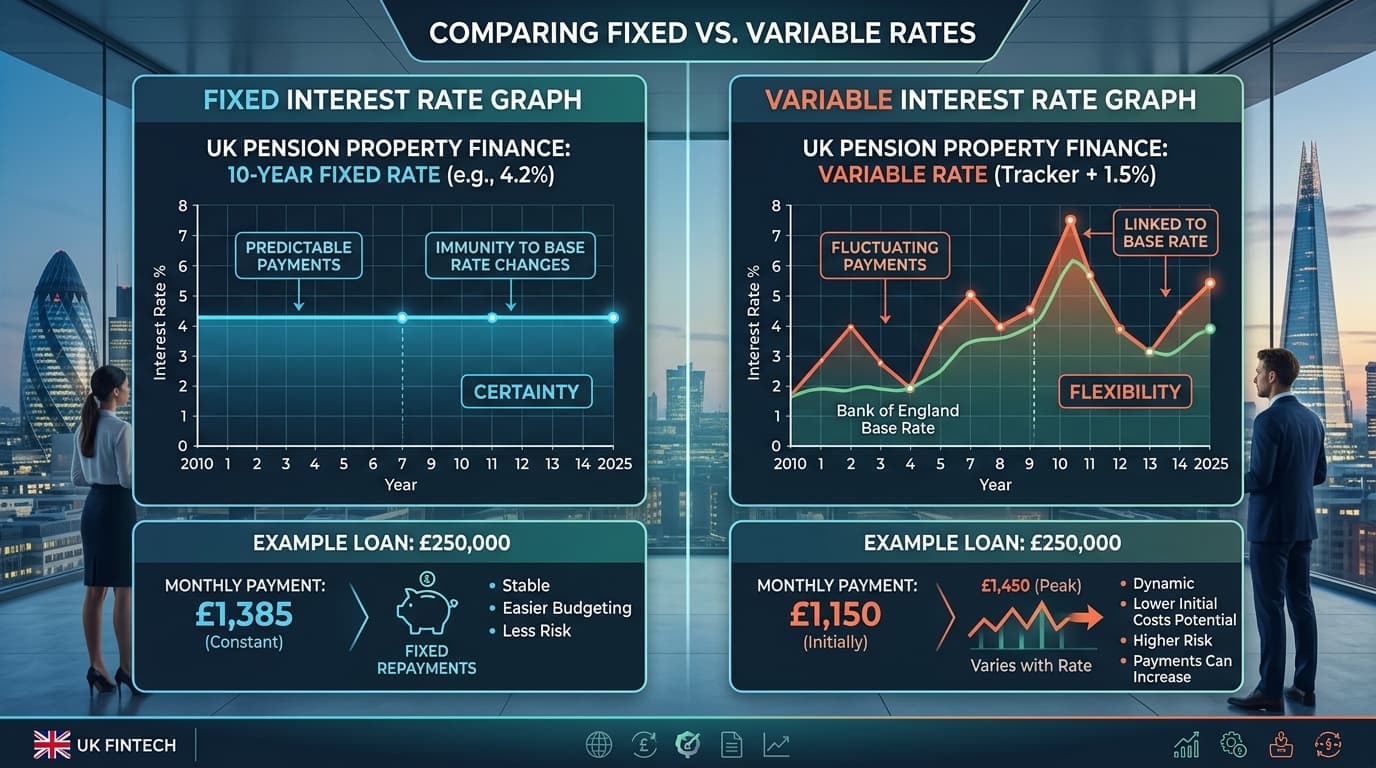

A fixed rate mortgage sets the interest rate for a defined period — typically two, three, or five years, though longer fixed periods of up to ten years are available from some lenders. During the fixed period, your monthly interest payment does not change regardless of what happens to base rates or market rates.

Advantages of Fixed Rates

- Payment certainty: You know exactly what the scheme will pay each month, which simplifies cash flow planning and ensures the rental income from the tenant comfortably covers the mortgage payment

- Protection against rate rises: If interest rates rise during the fixed period, your payment is unaffected

- Budgeting simplicity: Particularly useful for SSAS schemes with multiple members who need to plan around the scheme's cash flows

Disadvantages of Fixed Rates

- Early repayment charges (ERCs): Most fixed rate products carry significant ERCs if you repay early or switch to a different product during the fixed period — often 1-5% of the outstanding loan

- Rate risk on the upside: If base rates fall during the fixed period, you continue to pay the higher fixed rate while variable rate borrowers benefit from lower costs

- Higher initial rate: Fixed rates typically carry a small premium over equivalent variable rate products, reflecting the certainty they provide

Variable Rate SSAS Mortgages

Variable rate mortgages move with an underlying benchmark — typically the Bank of England Base Rate or SONIA. Your rate is expressed as a margin over this benchmark (e.g., "Base Rate + 2.50%"), and as the benchmark changes, so does your monthly payment.

Advantages of Variable Rates

- Flexibility: Variable rate products typically carry lower or no early repayment charges, meaning you can repay early or refinance without a significant penalty cost

- Rate falls benefit you immediately: When base rates fall, your payment falls in step

- Often lower initial rate: Variable rates frequently start below equivalent fixed rates

Disadvantages of Variable Rates

- Payment uncertainty: Your monthly payments can rise if base rates increase, which may create cash flow pressure if rental income is tightly matched to mortgage payments

- Planning complexity: Variable payments make longer-term scheme financial planning more complex

- Rate risk: In a rising rate environment, variable rate borrowers see their costs increase in real time

"In our experience, the fixed vs variable decision for SSAS schemes comes down to two questions: how much cash flow buffer does the scheme have, and how likely is the property to be refinanced or sold within the fixed period? If the answer to either question is 'not much' or 'very likely', variable usually makes more sense." — Matt Lenzie, Former Banker & Corporate Finance Partner

When Fixed Rates Suit a SSAS

Fixed rates are typically the right choice when:

- The SSAS's rental income from the property is closely matched to the mortgage payment, with limited cash flow buffer

- The scheme has multiple members who need certainty of scheme cash flows for planning purposes

- Interest rates are expected to rise or are at a cycle low

- You intend to hold the property for a long period without refinancing

- You are nearing the end of the SSAS's active investment phase and want to de-risk cash flows

When Variable Rates Suit a SSAS

Variable rates are typically more appropriate when:

- The scheme has strong cash flow surplus beyond the mortgage payment, providing a buffer against rate rises

- You expect to refinance, sell the property, or repay early within the next two to three years

- Interest rates are at a cycle high and expected to fall

- You value flexibility over certainty — perhaps because the property strategy is evolving

- The property is being purchased as a transitional investment pending a longer-term strategy

Comparing the Total Cost of Each Option

When comparing fixed and variable rate options, do not focus solely on the headline interest rate. The total cost of each option over your planned holding period includes:

- Interest paid over the period (based on the rate and any assumed future rate changes)

- Arrangement fees (often higher for fixed rate products)

- Early repayment charges (if applicable)

- Potential reversion rate after the fixed period ends

Our SSAS mortgage calculator can help you model these scenarios side by side. For a direct comparison of products currently available on the market, see our SSAS rate comparison guide.

The Reversion Rate Risk

One factor that fixed rate borrowers sometimes overlook is the reversion rate — the rate the mortgage reverts to when the fixed period ends. If the reversion rate is significantly higher than the prevailing market rate at that time, you may face a sharp increase in payments unless you refinance. Always check the reversion rate (and any associated fees) when comparing fixed rate products.

Key Takeaways

- Fixed rates provide payment certainty but carry ERCs and limited flexibility

- Variable rates offer flexibility and potential savings if rates fall, but expose the scheme to payment risk

- The right choice depends on scheme cash flows, expected holding period, and rate outlook

- Total cost over the holding period — including fees and potential ERCs — is a more complete comparison than headline rate alone

- Always check the reversion rate on fixed rate products

Get Expert Rate Advice for Your SSAS

Choosing the right rate structure is one of the most important financing decisions your scheme will make. Our team can present fixed and variable rate options from across our lender panel and help you evaluate the right choice for your specific circumstances.

Contact us for a rate comparison, or explore the SSAS mortgage rates explained guide for more background.

About the Author

Matt Lenzie

Former Banker & Corporate Finance Partner

Matt Lenzie is a former banker and corporate finance partner with extensive experience in pension-backed property transactions. He founded SSAS Property Finance to help company directors and trustees navigate the complexities of commercial property acquisition through Small Self-Administered Schemes.